Economía y Empresa

Japanese Economy

The Japanese Economy:

The Bubble Economy and the aftermath

By: Gilles PENOUILH

For INUI SENSEI Class

Summary: This paper is an intent to understand the evolution of the japanese economy during the last two decades. In the first part, we will have a look at the bubble economy, then we will see the period of crisis that followed. Finally, in the last chapter some solutions to the crisis will be discuss.

Introduction

Chapter One: The 80's or the Bubble Economy

I- The “Bubble Economy”, General facts

II - Closer look at the financial system during the “bubble economy”, and the cause of the crisis to come

Chapter two: The 90's, period of crisis

I The consequences of the “Bubble Economy”:

II Fiscal vs. Monetary Policy

Chapter III: The reforms

I - Why is the Traditional Growth Model Not Working Any More ?

II - Required Policies for Structural Reform

III - Reforms (monetary/fiscal policies to be done)

Conclusion

Introduction

The success of the japanese economy in the period of the afterwar is indeniable. It has gone from almost nothing to a vast exporting market invading the international trade markets with its new technologies. Thus, the economy of the country soon became reckoned as one of the most powerful and successful in terms of competitiveness and wellfare. Many people soon attributed Japan's success to a combination of factors:

Government-industry cooperation, a strong work ethic, mastery of high technology, and a comparatively small defense allocation (1% of GDP) have helped Japan advance with extraordinary rapidity to the rank of second most technologically powerful economy in the world after the US and third largest economy in the world. One characteristic of the economy is the working together of manufacturers, suppliers, and distributors in closely-knit groups called keiretsu. A second basic feature has been the guarantee of lifetime employment for a substantial portion of the urban labor force. Both features are now eroding. Industry, the most important sector of the economy, is heavily dependent on imported raw materials and fuels. The much smaller agricultural sector is highly subsidized and protected, with crop yields among the highest in the world.

This paper is an intent to analyse the causes of the actual crisis and to try to give some possible issues to that aftermath.

As a matter of fact, for three decades overall real economic growth had been spectacular: a 10% average in the 1960s, a 5% average in the 1970s, and a 4% average in the 1980s.

But that growth slowed markedly in the 1990s largely because of the aftereffects of overinvestment during the late 1980s and contractionary domestic policies intended to wring speculative excesses from the stock and real estate markets.

In later dates, the Government has been trying to revive economic growth but has met little success and was further hampered in late 2000 by the slowing of the US and Asian economies.

Pb: The crowding of habitable land area and the aging of the population are two major long-run problems. How can the Japanese economy exit this period of crisis ?

Chapter One: The 80's or the Bubble Economy

Throughout this chapter, we will see some aspects of the “bubble economy”, which lasted from 1987 to the beginning of the 90's. First of all, it could be convienient to give a brief definition of the so called “Bubble Economy”. It is the period during which speeding of the growth of japan's money supply, fueled massive increases in Japanese land and equity prices. The purpose of this chapter is to understand why it led to the crisis that Japan knows eversince 1990. So to speak, the crisis that happened in the early 90s has something to do with what had been done previously and this is precisely what we are going to see thereinafter.

I- The “Bubble Economy”, General facts

In the mid-1980s, Japan became the world's largest creditor and Tokyo a major international financial center. Four of the biggest banks in the world were Japanese at that time, and Japan had the world's largest insurance company, advertising firm, and stock market. In the remainder of the 1980s, Japan's financial and banking industries grew at unprecedented rates.

The main elements of Japan's financial system were much the same as those of other major industrialized nations: a commercial banking system, which accepted deposits, extended loans to businesses, and dealt in foreign exchange; specialized government owned financial institutions, which funded various sectors of the domestic economy; securities companies, which provided brokerage services, underwrote corporate and government securities, and dealt in securities markets; capital markets, which offered the means to finance public and private debt and to sell residual corporate ownership; and money markets, which offered banks a source of liquidity and provided the Bank of Japan with a tool to implement monetary policy.

Japan's traditional banking system was segmented into clearly defined components in the late 1980s: commercial banks (thirteen major and sixty-four smaller regional banks), long-term credit banks (seven), trust banks (seven), mutual loan and savings banks (sixty-nine), and various specialized financial institutions. During the 1980s, a rapidly growing group of nonbank operations, such as consumer loan, credit card, leasing, and real estate organizations, began performing some of the traditional functions of banks, such as the issuing of loans.

Japan's securities markets increased their volume of dealings rapidly during the late 1980s, led by Japan's rapidly expanding securities firms. There were three categories of securities companies in Japan, the first consisting of the "Big Four" securities houses (among the six largest such firms in the world): Nomura, Daiwa, Nikko, and Yamaichi. The Big Four played a key role in international financial transactions and were members of the New York Stock Exchange.

Japanese insurance companies became important leaders in international finance in the late 1980s. More than 90 percent of the population owned life insurance and the amount held per person was at least 50 percent greater than in the United States, for example. Many Japanese used insurance companies as savings vehicles. Insurance companies assets grew at a rate of more than 20 percent per year in the late 1980s. These assets permitted the companies to become major players in international money markets. (Nippon Life Insurance Company, the world's largest insurance firm, was reportedly the biggest single holder of United States Treasury securities in 1989.)

The Tokyo Securities and Stock Exchange became the largest in the world in 1988, in terms of the combined market value of outstanding shares and capitalization, while the Osaka Stock Exchange ranked third after those of Tokyo and New York. Although there are eight stock exchanges in Japan, the Tokyo Securities and Stock Exchange represented 83 percent of the nation's total equity in 1988. Of the 1,848 publicly traded domestic companies in Japan at the end of 1986, about 80 percent were listed on the Tokyo Securities and Stock Exchange.

Two developments in the late 1980s helped in the rapid expansion of the Tokyo Securities and Stock Exchange. The first was a change in the financing of company operations. Traditionally large firms obtained funding through bank loans rather than capital markets, but in the late 1980s they began to rely more on direct financing. The second development came in 1986 when the Tokyo exchange permitted non-Japanese brokerage firms to become members for the first time. So that by the year 1988 the exchange had sixteen foreign members.

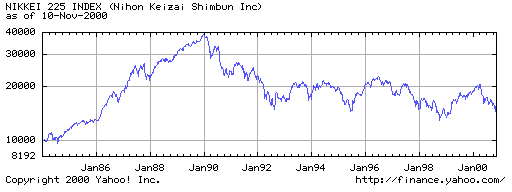

Japan's stock market dealings exploded in the 1980s, with increased trading volume and rapidly rising stock prices. During a six-month period in 1986, total trade volume on the Tokyo exchange increased by 250 percent (which is quite a big figure), with wild swings in the Nikkei. After the plunge of the New York Stock Exchange in October 1987, the Tokyo average dropped by 15 percent, but there was a sharp recovery by early 1988. In 1990 five types of securities were traded on the Tokyo exchange: stocks, bonds, investment trusts, rights, and warrants alone.

Japanese Stock market

II - Closer look at the financial system during the “bubble economy”, and the cause of the crisis to come

The most powerful institution in Japan is definitely, the Ministry of Finance (MOF). The power of the MOF has inhibited the development of true financial markets in Japan. Presently capital is allocated on the basis of who knows whom instead of economic effectiveness. The commercial success of Japanese manufacturing has led to Japanese banks of enormous wealth but without the corresponding level of financial skill and expertise. Japanese banks typically rely upon the guidance of the MOF and consequently do not exercise sufficient independent judgment and have not learned to cope with financial difficulties. Banks have lent heavily with land as collateral.

In 1985 interest rates on deposits began to be deregulated. Prior to that time bank were not allowed to pay interest on deposits.The removal of this prohibition led to competition between banks for deposits and hence to interest payments. Japanese banks did not raise interest rates they charged borrowers and offset the effect of the higher costs of their funds. They made up for the drop in their profits by selling the shares of stock they owned for a long time and counting the realized capital gains as profits. But because of the obligation of cross-holding of stock among the members of keiretsu they immediately bought back the shares at the new higher price. This meant that they were able to count the capital gains as a profit, but they had to pay tax on the capital gains. They thus experienced a net loss of cash flow on the operation. Furthermore a decline in the stock market then meant a disguised capital loss.

The Bank of International Settlements (BIS) has rules which are critical for Japanese banks. According to BIS rules, bank capital consists of two parts. Tier-one capital is the stockholders funds and retained earnings. Tier-two capital consists of such things as loan-loss reserves and "hidden assets." Forty five percent of unrealized capital gains on stocks can be counted as "hidden assets" and part of tier-two capital. This was a compromise of the BIS to accomdate Japanese banking. Some members of the BIS did not want to allow any unrealized capital gains to be counted as part of bank capital. Although counting unrealized capital gains accomodated the Japanese banking system, it made them vulnerable to price fluctuations in the stock market. If the stock market goes down then the Japanese banks must scurry to raise capital to meet BIS standard of an 8 percent ratio of capital to liabilities.

During the bull market in Japanese stocks banks issued new shares which allowed them to increase their assets. Between 1987 and 1989 city banks issued 6 trillion Yen of equity and equity-related securities. But when the Tokyo stock market crashed in 1990 these banks had a hard time maintaining the BIS required 8 percent capital ratio. Only one bank, Kyowa Bank, could maintain this ratio. The number of regional banks that could meet the 8 percent ratio declined from 50 in March of 1990 to 4 in September of that year.

During the "Bubble Economy" Japanese banks borrowed extensively in the Euro-dollar markets, 186 trillion Yen by June of 1990. Despite being the largest banks in the world these Japanese banks were having to pay a premium in their borrowing, the so-called "Japanese rate".

From the borrowed funds Japanese banks lent extensively. They opened American branches which earned very low rates of return, about 2 percent on equity. They did most of their lending in the peak of the American real estate market and consequently suffered extensive losses when property values declined and loans went bad.

The collapse of the Tokyo stock market collapsed the banks tier-two capital and put them under pressure to find capital. They no longer could find easy capital to borrow and had to liquidate many of their overseas holdings, often at a loss.

Japanese banks were also adversely affected by the decline of property values in Japan. In 1990 Japanese banks held about 22 percent of the mortgages in Japan. In addition, many of the loans to small businesses are backed by property and 75 percent of the banks lending is to small businesses.

There were other financial intermediaries in the property-backed loan market. The Housing Loan Corporation, a government agency, provides interest rate subsidized mortgages. Employers also sometimes provide subsidized home loans. There are also leasing companies, consumer-finance companies, and mortgage companies active in the mortgage market but these institutions are generally dependent from the banks for their funding so they represent the indirect participation of Japanese banks in the mortgage market.

In addition to the above financial institutions there are also secondary regional banks called sogo banks and shinkin banks. In Japan banks are not only not required to establish reserves for bad loans, they are effectively penalized for doing so. Setting aside funds to cover bad loans would reduce the tax liability of the bank and so the banks have to obtain permission from taxing authorities to create bad loan reserves. Consequently in 1991 Japanese banks had reserves of only 3 trillion Yen for total loans of 450 trillion Yen. Japanese banks tend not to report that a loan is in default because it makes the accounting profits look bad. Banks pressure the borrowers to come up with 30 percent of the interest owed because this allows them to avoid reporting their loans as being bad. This practice of not admitting problems or trying to solve them using gimmickry has become a concern of the Bank of Japan, the central bank of Japan.

The land market in Japan is heavily influenced by tax rules. Years ago, the Japanese government established high taxes on capital gains on land to discourage speculation. For any land held less than two years after purchase the capital gain is multiplied by 150 percent and this amount added to current income in computing the sellers income tax. If land is sold two to five years after its purchase then 100 percent of the capital gain is added to income for tax purposes. Effectively this is a 90 percent tax rate on property held less than two years, a 75 percent tax rate on property held two to five years, and a 50 percent tax rate on property held more than five years. This tax system discourages people from marketing land and consequently those who need land for some project find they have to pay exorbitant prices to get someone to part with it. Very little land changes hands and then as often as not to relatives. Consequently the valuation of land is artificially inflated. This artificial valuation of land would not be of much significance if it were not for the fact that people borrow money based upon their holdings of land. This begins to qualify for the term "astronomical." In November of 1991 the Ministry of Construction reported that houses and apartments in metropolitan Tokyo had in the preceding year lost 37 percent of their value and plots of land in the suburb of Saitama had lost 41 percent. The bubble in property values would not have been significant except for the fact that the use of land as collateral for loans and the fact that the taxing authorities tend to use those peak prices in valuing property subject to the inheritance tax.

For instance, during the "Bubble Econonmy" there was a uniquely Japanese episode of speculation in golf club memberships.

Life insurance companies around the world are partly involved in providing insurance against risk and partly in providing savings programs. In both activities they end up having to invest heavily in financial securities. Life insurance companies in Japan own more stock than does any other type of financial institution. For example, in 1990 they owned 13 percent of the stock on the Tokyo stock market compared to 9 percent held by banks. The rates of return on managing their portfolios of stock could be quite misleading for them. There is a special problem for Japanese insurance companies. Japanese law requires that they pay policyholders out of income rather than capital gains. This has led to some strange financial operations, such as trading stock for bonds that paid high interest but gave little payment at maturity. Japanese insurance companies were at risk in the property market also. Six percent of insurance assets were property and many of their domestic loans were backed by property. When Japanese insurance companies became involved in foreign investment they subjected themselves to considerable risk. One such risk had to do with fluctuations in exchange rates.

Despite the recent economic problems of Japan, the leaders take the position that Japan has developed a special type of economy that is in between free market capitalism and socialism but at the same time, supperior to both.

Chapter two: The 90's, period of crisis

As we saw over the first chapter of this essay, the « bubble economy » of the 80's would drive Japan right to the point it reached at the beginning of the last decade. As a matter of fact, the way people played he economy was obviously going to lead to an economic problem.

Only a few years before, Japan was viewed as an exemplary economic success story and a model of successful economic long-run growth. People talked of “Japan Inc.” and the Japanese growth model was being suggested as a case study to be followed by other developing and developed countries. As we saw, this general thought was due to the fact that the country had known a dramatic growth during more than 3 decades.

But, as we often refer to: after a boum comes the crisis. As a matter of fact, it is not rare in economy to see a national economy following the scheme of the so called business cycle. In other words, there are some periods of growth and some periods of crisis. Thus, in the case of Japan it seems a little bit different. As I pointed out in the first chapter, something was going wrong in the financial system Japan supported way before the crisis.

However, I will argue that the Japanese economy suffers of severe problems that are not only cyclical but more structural in nature. Such structural problems are the most serious impediments to entrepreneurship, economic dynamism, which will be discuss a little bit further, in Chapter 3.

For now, I wish to expose the result of the “bubble economy” in the japanese economy during the 90's. I will first start with an overview of the current Japanese macroeconomic problems before moving to the more structural issues (fiscal/monetary policy).

I The consequences of the “Bubble Economy”:

A- The “Bubble economy”:

- Low interest rates (about 0%)

- Firms overborrowed

- Banks overlent

- Asset prices proved unrealistic

- Banks couldn't collect on their loans

- But pricing long-lived assets was hard

-Real estate grew faster than economy

-Stock prices grew faster than economy

-Growth industries grew very fast indeed!!

B- Consequences:

- Interest rates can't be pushed below 0%

- Falling prices falling

- Banks (rightly) fear bad assets

- Outstanding loans shrinking

- “Liquidity Trap”

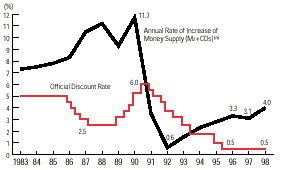

As you can see on the fig., the year 1990 points out quite a big gap in the Japanese Money supply.

II Fiscal vs. Monetary Policy

I will now consider fiscal and monetary policy's effectiveness in attaining growth with respect to the current situation in the Japanese economy.

A- Fiscal Policy

In the last 10 years, Japan has put together a string of fiscal stimulus packages that have caused the economy to grow, but not in autonomy. 2/3 of that growth was caused by the actual spending of the yen stipulated in the package. Only 1/3 of the growth came from growth caused by externalities like higher level of aggregate income, consumption, etc. The failure of fiscal policy in a flexible exchange rate system has been examined by Keynes. In the case of a recession, short run equilibrium settles below the level of full employment. This tells us that the japanese production resources (capital and labor, etc) aren't being used in the most efficient manner. So in this case, government intervention is seen as the key to moving out of the recession.

The rise in consumption by the government acts to stimulate the domestic interest rates. As those interest rates rise above the world level this will induce an appropriate rise in the inflow of capital. Because of the higher demand of the yen (domestic currency) it will begin to appreciate against other currencies. The export sector will be hit the hardest as their products become relatively more expensive versus other goods. As the export sector becomes less competitive, cheaper imports will begin to infiltrate the economy, thus undermining the domestic sector. So, although the government raises its consumption, the decline of the export industries and the increased imports will tend to offset the gains. With a fixed money supply, the government is just changing the composition of aggregate consumption by crowding out the private sector's consumption and investment. As interest rates rise, this will make borrowing money and investing more expensive. So, as the negative effects of an appreciation of the domestic currency drives the economy back to the initial equilibrium point.

As the asset bubble deflated and Japan began to inject fiscal stimulus, the yen did appreciate for 5 consecutive years from 1991-1990. The yen climbed as high as 85 yen to the dollar...way up from 360 yen to the dollar. Despite the appreciation, the trade surplus remained in tact for two reasons...innovation by the exporting industries and the tight business ties within the keiretsu.

The exporting industries found new ways to cut costs. They shifted production to the US where the Yen was strong and therefore foreign asset prices relatively cheap. Japanese auto manufacturers such as Toyota and Honda were able to avoid losses in foreign exchange by assembling the cars cheaply in America and other dollar-pegged countries in Asia. This served to offset rising yen-related costs as production moved offshore. To cut costs even further production of commodity-type goods declined. Commodity-type goods are characterized as being very price sensitive. Goods that have little or no differentiation except for the price are considered part of this group. Textiles, metals and agricultural goods are examples of this. As sales declined, more of those resources began to shift into what is called the high-value goods. These goods' demand is less sensitive to price changes as it is with quality and technology. Electrical machinery, and transportation equipment, etc are examples of this. Because not every country is able to produce high-value goods, they are seen as price makers, whereas the former are referred to as price takers.

Keiretsu ties have been very effective in keeping lower priced imports from entering the Japanese market. The keiretsu are a mixture of vertical and horizontal integrated companies. A bank is at the center to provide finance and support for investments. It is standard to have input manufacturers of an export good be part of the export industry's keiretsu group. Auto parts manufacturers are often part of the same group as their auto manufacturer. The auto parts company's demand will come largely from this auto manufacturer in return for not buying cheaper foreign auto parts. Because the companies within the keiretsu hold a certain percentage of each other companies' stock, it is in their best interest to buy from their member companies to keep them afloat and keep the value of the stock high. This has been successful in keeping out imports. Profit margins are generally lower, but that is an insurance premium during times of economic hardship.

In 1991, there was a fiscal surplus of 3% of GDP, and government debt was below 10% of GDP. By 1996, however a 1 ½ % budget surplus was turned into a 3 ½ % budget deficit. This was mainly caused by 6 different fiscal stimulus plans implemented throughout the first half of the decade. In 1996, as the debts mounted, Japan felt that the recent growth in the economy was an indication of self sustain-ability and decided to consolidate the debt and begin to pay it off. The government implemented three policies.

The social security tax was raised in 1996.

A tax cut of 25% of GDP was taken away.

The consumption tax was raised from 3% to 5%. During this time 3% of what made up GDP was taken away from the economy. The Japanese government was criticized not for trying to rid itself of debt, but in the manner in which it went about doing it. At the time key policy decisions were made, Japan had experienced only about a year of solid recovery after four years of near stagnation. With that year of recovery boosted by substantial fiscal stimulus, there was reason to question whether economic expansion had yet been put on a strong, self sustaining basis, capable of bearing a sudden withdrawal of fiscal support. The need for fiscal consolidation over the medium and longer term was undisputed, and there were good reasons to start, at a gradual pace as soon as possible." Because politically, the shift from consolidation to once again fiscal easing was unattractive, it would have been hard to convince law makers of its necessity. This delayed the reaction to the Asian Crisis. This is why three major institutions failed in November of 1997 and there was no monetary and fiscal response until April of 1998.

Overall, fiscal policy's effectiveness has been hampered by the deflation in the price of assets, the appreciation of the exchange rate from 1991-1996, the credit crunch brought on by the debt laden banks and a severe decline in the confidence in the banking industry. It has been noticed by IMF officials that the government spending multiplier is between 1-1.2, whereas the tax multiplier is only .5-.8. This may seem at face value that government spending is the more effective tool, however tax cuts better fulfill the role in the long term growth model.

B- Monetary Policy

Monetary policy is viewed as effective in the short run in boosting output in an ailing economy. Investors looking for higher returns on their investments look outside the country for a higher interest rate and sells domestic currency which will depreciate the value, making the export sector more competitive. This in turn makes foreign goods relatively more expensive and consumption shifts to domestic goods. This shift in consumption coupled with a competitive increase in exports leads to an increase in aggregate income and an increased demand overall.

The ability for expansionary monetary policy has been greatly diminished in recent years. The official discount rate was lowered from 6% in 1991 to a level of 4,5 % in 1992. Again in 1993 it was lowered to 1,25 %. The last time it was lowered was in 1995 when interest rates were targeted at an all time world low .5%. Short term bank lending rates haven't declined as far. Most banks are lending at a current rate of 7%. However, lowering the interest rates aren't the only condition to easing monetary conditions. As inflation was falling, the real interest rates were falling as well, but at a rate slower to that of the nominal interest rates. So, real interest rates were higher than the nominal rates.

Also, in the aftermath of the bubble economy, deflated asset and real estate prices resulted in a lot of bad debts. So, as nominal interest rates declined, to protect themselves, banks lowered their lending rates at a much slower pace.

In 1993 and 1995, as signs of growth entered economic indicators, monetary policy was quickly tightened to lessen any signs of inflation. This caused the yen to continue to rise once again. As this began to take place again, the Bank of Japan was too late in lowering interest rates as economic conditions began to further deteriorate. It was a case of "too little too late".

Expected inflation within an economy has both positive and negative outcomes.

Inflation would cause real interest rates to decline. In today's Japanese economy inflationary expectations would push real interest rates below zero, in effect making it profitable to borrow money and either spend or invest.

Higher product prices would stimulate growth in production. Producers would see the potential for higher profits. With real wages decreasing in the short term due to contractual negotiations done in the past, producers would see an increase in worker productivity in the short run...or at least until new wage contracts are worked out.

Expected higher future prices would alter future consumption (present savings) to present consumption.

There are however detractions to the use of monetary policy. A weak yen will cause other countries to tighten their monetary policy, which will offset some of the benefits to japan. Household confidence could be undermined because of the stigma of inflation as bad. This could lead to further declines in spending. Business investment could be muted by other external factors which detract from the economy, such as the bad debt crisis within Japanese banks. So in conjunction with raising inflationary expectations, it is necessary to also solidify external markers of confidence within the economy such as banks, stock market, government, etc while raising incentives to spend and invest.

Conclusion to chapter II:

The crucial question is: is the experience of the 1990s just a temporary and cyclical blip that does not put in question the old growth model or is the traditional economic regime now partially flawed and in need of structural change and reform ?

I will argue that the latter is the case. What has changed in the last decade to make obsolete the old growth model ?

Chapter III: The reforms

In later dates, the Government has been trying to revive economic growth but has met little success and was further hampered in late 2000 by the slowing of the US and Asian economies.

Pb: The crowding of habitable land area and the aging of the population are two major long-run problems. How can the Japanese economy exit this period of crisis ?

I - Why is the Traditional Growth Model Not Working Any More ?

Many authors have advanced the hypothesis that higher growth in the new global economy is associated with greater risk-taking, dynamic entrepreneurship and more aggressive competition rather than the low risk model of the last few decades. The old growth model does not work anymore because of four fundamental new trends in the world economy:

1. Structural change in the nature of technological innovation.

2. Greater global trade competition

3. Deregulation that is fostering competition

4. Corporate restructuring.

Lets consider these trends in more detail.

1. Structural change in the nature of technological innovation.

First of all, it has been argued that the nature of technological innovation has changed. From the 1950s until the early 1980s, innovation took the forms of already existing technologies and goods that had to be improved in quality (examples are: cars, stereo systems, photographic equipment, other consumer electronics goods). The Japanese were best at doing this as being the best in “process innovation”, “quality improvement” and “product imitation”.

Today, technological innovation is very different because of qualitative changes in technologies and the rapid appearance of new and very different products (computers, software, Internet and information technologies, advanced chip technologies, telecommunication goods and services, new financial instruments and services). These products are appearing and changing at such at dizzying pace that an imitator cannot catch up with the product and technological leaders. The product cycle of innovation has become drastically shorter. Extreme example: the Internet Browsers and the war between Microsoft and Netscape. So, today you either innovate and remain on the cutting edge of the technological wave or you will remain forever behind.

To put it bluntly, a mainstream view in the United States right now is that in all these new technologies and products Japan is completely behind the US and will be unable to catch up.

2. Greater global trade competition

Increased global trade has led to global competition and the need for industrial restructuring.

Japan until recently did not liberalized trade as much and delayed this structural adjustment. The strong Yen trend until 1994 led to significant import penetration, loss of manufacturing jobs and the export of jobs to other East Asian countries through a major process of outward FDI. However, domestic corporate restructuring has been very slow. In this regard, the significant fall of the Yen since 1995 is a bad omen for Japan because, while giving short-run breathing room to the battered industrial sector, it dilutes the incentives for structural restructuring and slows significantly the drive to change. Also, the regulated and non-competitive non-traded sector of services has not been affected by the external trade liberalization pressures as much as the traded manufacturing sector. So the global trade pressure to reform has not hit the service sector.

3. Deregulation policies causing competition

While there is a lot of talk and policy proposals for major deregulation of the economy in Japan, this has not occurred yet in any significant scale.

4. Corporate restructuring

The combined forces of technological change, trade competition, deregulation of the economy led to major corporate restructuring in the US that took the forms of

a. Re-engineering

b. Out-Sourcing

c. Large scale Downsizing of firms

d. Massive corporate control restructuring through Mergers and Acquisitions

Because of this dramatic restructuring over the last decade the US economy is now highly productive, with low labor costs, highly innovative and very competitive in world markets. Of course, there were very high social costs of this restructuring process first for blue-collars and now for white collars and managers:

a. Major job turnover

b. Great job insecurity

c. Need for disrupting occupational and regional mobility

d. Depressed real wages for average workers

e. Significant increase in income and wealth inequality

However, such corporate restructuring has led to higher productivity growth, a resurgence of manufacturing, high employment growth and low structural unemployment rates.

In Japan instead the strong Yen of the early 1990 led to outward FDI, the hollowing out of the manufacturing sector, significant jobs losses but no major structural reform of the economy. Reform has been very slow because of the following factors:

a. The lack of major economic deregulation

b. The persistency of oligopolistic structures and lack of market competition

c. The still relatively protective trade policies and inward FDI policies

d. The recent weakness of the Yen

While these factors have sheltered Japan in the short-run from the brutal logic of the new word economy, they have also significantly slowed down the pressures for reform. Therefore deindustrialization in Japan may become more permanent than transitory .

In Europe, there is a welfare system where the “insiders” are guaranteed jobs and high real wages but they have to pay high taxes to support the “outsiders” (i.e. unemployed). While differing from Europe in many respects, Japan has a number of similar structural rigidities in labor markets.

Probably, the different social culture and history of Japan suggests that Japan will not and should not follow the brutal “Wild-West” American model of restructuring and reform. However, there is need in Japan for major structural reforms and economic deregulation in order to foster entrepreneurship, risk taking, innovation and long-run growth. Japan will have to find its own national path to reform and change but the process is going to be painful. Also, delaying these reforms will not help because short-run reduction of the pain might lead to more serious problems in the long-run as the persistence of the recession for over four years now suggest.

II - Required Policies for Structural Reform

The policy changes needed to deregulate the economy and foster competition and entrepreneurship are now quite well know and object of serious policy debate in Japan. We can summarize them as:

1. Financial markets liberalization (important role of financial markets for growth):

- Financial restructuring of the banks and reform of banks' supervision activities

- Liberalization of insurance markets and services

- Expansion of shareholder rights

- Improvement of disclosure procedures

- Creation of an independent institution similar to the US Securities and Exchange Commission

- Develop venture capital institutions

- Allow the formation of holding companies.

2. Deregulation and fostering of competition in domestic markets:

- Improve services productivity through deregulation and competition. Right now the low productivity service sector is a main drag on the economy and negatively affects the competitiveness of the export sector as well. Sectors requiring deregulation include retail, transportation, telecommunications, telephone service.

Example: you can't really tap into the Internet with an archaic phone network

- Foster competition through further trade liberalization and avoid further Yen depreciation

- Reduce oligopolies with aggressive competition policies.

Administrative and political reform:

- Reduce the powers of the bureaucracy

- Reduce the power of the Ministry of Finance and dismantle it into several smaller agencies

- Regional decentralization to reduce central power

III - Reforms (monetary/fiscal policies to be done)

The government of Prime Minister Junichiro Koizumi should be commended for its commitment to implementing wide-ranging structural reforms. Given its victory in the recent Upper House elections, Mr. Koizumi and his party have an opportunity to implement this agenda and bring about real change for the better in the Japanese economy.

Not everyone agrees, however, that this is the right time to press ahead with reforms, or even that such reforms will help solve Japan's economic problems. Some commentators have suggested that reforms be delayed because of the weakening domestic economy and the uncertain outlook for global growth.

There is no denying that lack of demand is a problem and that macroeconomic policies have an important role to play. But would more expansionary macroeconomic policies by themselves restore strong, sustainable growth? The answer is no. Such policies have been pursued for much of the last decade without successfully reinvigorating the economy.

Structural problems lie at the heart of Japan's economic difficulties and a sustained rebound in private demand will remain elusive until these factors are decisively addressed. For more than a decade Japan has adjusted too slowly to the forces of globalization, lagging behind in innovation and productivity growth. The country must now remove the obstacles to efficiency in the domestic sectors of the economy, unwind the excess capacity and debt that was built up during the bubble years, and curb the rapid expansion of public-sector debt.

The government, therefore, needs to move ahead with reforms. Delaying or watering down the program will only prolong economic weakness and increase the risk of crisis. As an absolute top priority, the problems in the banking sector must be dealt with in a decisive manner. The government's April policy package to accelerate the disposal of bad loans is a welcome initiative. The measures need to be vigorously implemented and extended to all deposit-taking institutions not just the major banks.

However, despite this initiative and the progress made by the Financial Services Agency in strengthening its surveillance of the banking system, there still remains considerable uncertainty about the size of the bad loan problem and the adequacy of banks provisions against these loans. Until the scale of the problem is fully recognized, a final resolution will remain difficult to attain.

An important first step, therefore, will be to undertake a complete assessment of the scale of the bad-loan problem. To accomplish this, banks will need to further strengthen their credit assessments and adopt a more forward-looking approach to loan classification and provisioning. This is particularly important in the current environment of weak growth and continuing deflation where the likelihood of a loan becoming nonperforming is higher than under more favorable economic conditions.

Japan's recent decision to participate in the International Monetary Fund's Financial Sector Assessment Program, an existing monitoring program in conjunction with the World Bank, will contribute to this effort by helping to achieve a better understanding of the key issues faced by its banking industry. Under this program, the IMF has already assessed several dozen countries, including Canada.

Were the scale of the nonperforming loans to be significantly larger than currently recognized by the banks, additional provisions would be needed. This, of course, would adversely impact bank capital. In such a situation, public capital injections targeted at weak but viable institutions may be necessary to restore bank capital to adequate levels, maintain systemic confidence in the banking system and avoid a credit crunch that would further worsen the current economic situation. Ways would have to be found to minimize moral hazard associated with public money injections.

In other areas, addressing concerns about the sustainability of government and social-security finances should be high on the reform agenda. Fiscal reforms are necessary to underpin a credible, medium-term fiscal consolidation strategy —including a reduction in public works spending, reforms of pension and medical care programs, and an end to the practice of earmarking revenues in advance for specific purposes.

At the same time, decisions on when to start the process of fiscal reform, and how quickly to pursue it, need to be made with care; the weak economy and disposal of bad loans and corporate restructuring are likely to have a negative impact on growth and employment in the short term. Thus, while establishing a credible framework for medium-term fiscal consolidation is important, the government should avoid an abrupt withdrawal of stimulus so long as economic activity is weak. Indications that the government will introduce a supplementary budget later this year to expand the social safety net are welcome.

With regard to monetary policy, the Bank of Japan has aparently made a good decision to raise its quantitative target and increase its purchases of Japanese government bonds. Further measures are still likely to be necessary, however, and the effectiveness of policy would be enhanced if the Bank of Japan clearly specified a reasonable timeframe for eliminating deflation. Monetary policy along these lines should contribute to stronger economic activity by counteracting deflationary expectations and boosting domestic asset prices. Such a policy could also result in a weakening of the yen. But regional concerns about a weaker Japanese currency are likely to be markedly less than during the 1997-98 Asian financial crisis, given the adoption of flexible exchange rates by many countries and healthier external-debt profiles throughout the region.

The Japanese government also needs to introduce measures to strengthen the regulatory structure, reduce the role of public enterprises in the economy, improve corporate governance, increase labor market flexibility, and revitalize the real-estate market. Such policies will be important to generate new investment and employment opportunities, and raise productivity growth over the medium term.

Implementing these reforms will not be easy, but bold measures are needed to return the economy to strong, sustained growth. The past decade has shown the perils of delay. Now is the time to act.

Concluding on chapter III:

Will Japan be successful in facing these challenges ? There are reasons for both optimism and pessimism.

On the negative side:

1. Historically Japan reformed only after major crisis that broke the deadlock in society in favor of drastic reform. Today instead there is stagnation but not crisis.

2. The Yen is now still a bit weak and this delays the incentive to reform.

3. The big corporations (Sony, Honda, etc.) are very international and their fortunes depend less on the success of the Japanese economy; they have now less at stake if reform does not occur.

On the other side, there is reason for optimism:

1. History shows Japan's ability to reform and adapt fast in periods of crisis (examples are the Meiji Restoration and the Post-War World II development).

2. There is significant pressure (in the business sector and urban classes) for economic reform, deregulation and more competition.

3. The official policy program of the current government recognizes the need for urgent administrative and economic reforms.

4. The Japanese have repeatedly shown to be hard working, creative, willing to sacrifice personal interest for the collective goods, and willing to respond to challenges.

Conclusion

Throughout this short paper, we've seen the different steps of the Japanese economy over the last two decades. Japan has gone from a period of real growth, to a period of deep crisis and stagnation.

What is needed now is a comprehensive and transparent approach that would leverage the use of public funds to ensure that the bad debt problem is finally put behind and the banking system restored to profitability and a sound capital position. Essential ingredients of this approach include:

- early identification and prompt closure of insolvent institutions;

- aggressive efforts to dispose of problem loans;

- linking future injections of public funds to strong restructuring plans, including a

requirement to raise funds from the market;

- an end to regulatory forbearance in recognizing the extent of bad loans;

- adoption of international disclosure standards;

- and a large increase in resources for the new financial supervision authority, more than currently envisaged, to allow it to fulfill its mandate.

There is a lot to be done. It is not easy. But such measures are being taken in other countries, some of them in crisis, in this region and elsewhere, to deal with banking sector problems. There is no advantage to further delay. Those delays have contributed to the sustained period of slow growth in Japan, and they should not be tolerated any longer.

One more word on the need for transparency. In both the banking and fiscal areas, problems have persisted in part because of a lack of transparency. It is always difficult to work out what precisely is included in a fiscal package in Japan and this contributed to the miscalculation of the impacts of the tax increase in 1997. And the lack of transparency in the financial sector has also allowed this problem to linger for far too long. The need for transparency is one of the key lessons we have drawn from the Asian crisis, and the point applies to Japan too.

SOURCES OF INFORMATION

- Jacques Gravereau, “Le Japon au Xxe Siècle”, Edition augmentée 1994-

-David Flath, “The japanese economy”, Oxford University press 2000-

-Instituto Español de Comercio Exterior (ICEX) : http://www.icex.es/fichas/japon

-“The Evolution of the Japanese financial system and monetary policy”: http://netec.wustl.edu/BibEc/data/

Final Paper : The Japanese Economy in the 80's and the 90's

12

{kind=link}

Descargar

| Enviado por: | Mac Gilles |

| Idioma: | inglés |

| País: | México |

Todos los derechos reservados.