Administración y Dirección de Empresas

Quality cost

Quality costs introduction

Quality costs are one of the most important things within a company, speaking in profit terms. These costs must be at the same time, effective and cheap and as a result, customers will be completely satisfied. This is the base of every company and business, we desire to earn money as much as possible, offering to customers guarantees and satisfaction but to achieve these aims a sequence of steps must be followed, defined as cost of quality where different costs arise such as prevention cost, appraisal cost, and finally, failure costs.

The relationship between quality and cost implies that as quality rise, the cost rises too, and consequently the price of the product increases.

The customer is only willing to pay more for the product if the quality is proportional. Therefore the main task of quality control is to reach the level of quality, which maximises profit.

It is compulsory to define quality cost if we want to know what we are pursuing. Quality cost can be defined as follows:

“Quality cost are costs associated with making defective product”(Groocock ; The Cost of Quality).

As we mentioned above, prevention, appraisal and failure are the three categories, which embrace quality costs.

Failure includes scrap, rework as well as warranty costs, appraisal contains inspection and test costs, the activities related to prevent defectives belong to prevention category. Appraisal also includes those costs, which do not fall within any of the four categories.

Some advantages and disadvantages could be found categorizing quality costs.

On the one hand, among advantages, the attention should be drawn in the point that quality costs make accounting process easier. Furthermore, to make easier the classification of failure costs, they are subdivided in two subcategories; external and internal being external cost, more serious.

Focusing on quality costs reports, their best advantage is problems could be detected easier; consequently appropriate resources can be applied to its solution; moreover, some clear objectives and targets could be set, motivating people to reach them.

On the other hand it is undesirable to categorize quality cost as Groocock argues in “The cost of quality” due to:

1-It is not easy to differentiate which costs belong to each department.

2-If results are not like we expected, to identify the responsible people, could be a difficult task.

3-The quality cost definition is opposite to de idea of categorization.

Background

Quality is not a new term, it began at the same time as traditional jobs, when the customer placed an order to the artisan, and the artisan's work was according, to the requirements or needs specified by the buyer.

There was a direct communication between buyer and seller, as a result the quality was high but at the same time, the cost was high.

Gradually, industrial production burst into market and took the place of artisans, moreover mass production appeared and consequently the costs dropped drastically due to the fact of manufacturing with standard pieces and the appearance of production chains. Chains of production were problematic, because when the piece did not fit the requirements of the buyer, it was destroyed or considered scrap.

Therefore the first definition of quality arose;” requirement's fit”.

From that time companies needed departments of control of quality, because lack of quality was too expensive.

In the last few yeas, total quality has spread widely as a management tool within organizations, both public and private.

Quality could be considered as a philosophy of integration of the different activities and department of the company.

Quality means efficiency and effectiveness coupled with the reductions of costs and the increase of profitability. When we speak about total quality a new concept called “the intern customer” appears. All the staff is involved in the process of quality, and the product or services must be transferred from any department to another, without any failure. The supplier helps the customer to express customers' needs and them the supplier tries to satisfy as much as possible these requirements.

The larger is the chain of production, the less successful is the achievement of quality, it means that the commitment of all the people within the company is essential. If any link of the chain fails, the quality and effectiveness decreases.

But the needs of quality arise mainly due to the fact that, as business world is getting smaller, because of advance technology and cheaper air travel, companies must be aware of the competition increase, and in order to stay or remain ahead of the competition, their efforts should be greater as time goes by.

Obviously in order to study quality cost, first of all, the definition of quality must be known. Several definitions can be found, one of the most appropriate is “the totality of features and characteristics of a product, process or service that bear on its ability to satisfy stated or implied needs”.

In our case,”Stardust Computer Games” was founded in 1996,it means in terms of quality that this is a new company, having some advantages and disadvantages.

Concerning to advantages, it can be claim that the company does not have some bad habits and it is easier to implement a quality system due to the fact that people are less reluctant to changes within the organisation.

On the other hand some disadvantages arise, related to the wealth of the company and it does not have enough experience yet to know accurately what customers want.

We have to consider that our product is for children ,but the price is too high ,therefore however parents or who invest the money must be persuaded as well.

Actual calculations

The actual quality costs for stardust computer games for a year are as follow:

Two different costs could be found within quality cost:

-Cost of compliance-consist of prevention and appraisal costs

-Cost of non compliance-consist of internal and external failure costs.

The following costs have to be classified in the different categories seen above.

Firstly among the assets of the company, some of them are ignored as they are non costs of quality such as coffee maker, soldering irons, workbenches, photocopier, carpets&curtains , jigs&fixtures, company car. On the contrary IC tester, micrometers, multimeters , test bays could be considered as appraisal costs as they measure however the results either of the quality or of the customers requirements or of the quality of products .The total amount is £33,800,but we have to take into account the period of depreciation, it means to share the total cost of each asset among years of live of the asset. As a result the definitive total cost is £11,133.26 Appraisal costs are related to inspection and testing, either at the arriving of products or throughout the process or a the final stage.

Both of manufacturing scrap and obsolete and surplus stock belong to internal cost.

As they are considered a typical cost of the month, we have to calculate the total amount of the year, so that through the monthly amount, the annual amount has to be calculated, multiplying by 12.

Therefore the obtained figures are £13,074 and £693.6 for manufacturing scrap and obsolete and surplus stock respectively. The costs occurred while the product is still in the company's possession are regarded as internal costs. Either defective products or correcting defectives could cause these kinds of costs. In the case of stardust company both manufacturing scrap and obsolete and surplus stock take place while the products belong to the company, therefore this is the reason why they are considered internal costs.

Next, customer returns have to be classified, placing them in the external cost category. They are defined, as external costs due to these costs appear having transferred the product to customer; usually these costs are a result of warranty charges. The total amount of customer returns is (£1475.9 multiplied by 12) £17,710.8.

The next costs, which have to be taken into account, are salary costs. First of all the number of workers belonging to each stage of quality costs must be identified.

Respect to prevention activities, several departments can be found such as training, new design and quality systems. All these departments have in common that they try to ensure, things are right first time. In all we have 7 workers, earning each one £20,000 per year.

Concerning to appraisal we have 7.5 workers belonging to quality control, provision of equipment, inspection and finally test operators. This last department has 4 workers, 3 of them working for appraisal and one for internal.

To find out this the test report must be used, as we can see, 25% of the tests failed so 1 in 4 workers belong to internal costs and 3 to appraisal costs.

Apart from the internal cost of this worker, we should not forget to take into account quality investigation and rework departments. In all they have four workers.

Finally external cost needs one department called returns with one worker.

Another cost, which can be founded in the information provided, is the order cancelled .It must be considered as a internal cost due to the fact that the products remain in the company's possession .The cost considered is not £40 each product, because this is just the selling price, actually the estimate cost is about 40% of £40 each. The total amount reaches £1600(0.4*£40*100).

Respect to the city bank's letter, a new cost has to be faced, our account is overdrawn and there is a cost of £3,432 which comes from the different between £5,432 and £2,000.It could be considered as internal cost, because it is a consequence of the nasty planning, of the financial needs by the company.

Finally there is a cost associated with rework due to non conforming materials from suppliers .To calculate the board's cost we have to multiply 20 pence by 240(number of days in a year) and again multiply by 675(the number of boards manufactured each day). The cost rises to £32400.

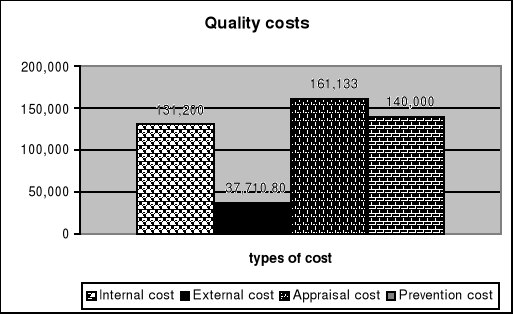

Therefore the total cost is:

| Internal cost | |

| -Manufacturing scrap | £13,074 |

| -Obsolete and surplus stock | £693.60 |

| -Salaries | £80,000 |

| -Order cancelled | £1,600 |

| -Overdrawn | £3,432 |

| -Rework | £32,400 |

| £131,200 | |

| External cost | |

| -Customer returns | £17,710.80 |

| -Salaries | £20,000 |

| £37,710.80 | |

| Appraisal cost | |

| -Assets | £11,133 |

| -Salaries | £150,000 |

| £161,133 | |

| Prevention cost | |

| -Salaries | £140,000 |

| TOTAL COST | £470,044 |

How to prevent cost of quality

There are three approaches to commit employees with quality:

1-Quality circles: it is an approach, which enables employees to be more involved in the decisions taken in the company. This managerial philosophy encourages employees to solve their own job related problems in an organised way.

The key feature of this approach is that, people are more involved, but at the same time they do not have pressure, in other words this is a voluntary process at all levels of the organisation.

Quality circles consist of a group of people, who meet together regularly, to identify, analyse and solve their work problems.

Among the advantages of this practice, we could find:

-Improvement and development of enterprise

-Happy working environment.

-Human capabilities and skills more developed.

-Participation by all.

-Creativity

-Quality consciousness.

In our company it means the communication among the 50 employees, and the contribution of ideas, because almost all of them have contact with children and then, they know what they want.

2-quality of work life: this is based in participation, when it is encouraged the perception of quality by the worker rises.

There are different ways to obtain work quality:

Improved co-operation between departments: The better is the internal communication, the more encouraged people are to learn about other departments.

Employee involvement in suggesting improvements: new ideas from employees must be fostered, offering rewards to involved people.

Improved security: the feeling of ownership makes people feel appreciated and consequently they are alert to possible thefts.

Reduced staff turnover: organizations with good reputation at staff relationships are more appreciated.

3-Conscience and responsibility: For the achievement of quality is essential, the involvement of the every member of the staff and, the commitment with quality, basic for the quality control.

The commitment must be based in a dynamic quality system and in an organizational framework, which leads the company to commitment and the administration of quality. The quality commitment is a endless process with different stages or dimensions. This process is basic for the quality control and the total quality systems.

For Stardust company this point is extremely important, since the company is new and it must reach the customer's confidence and goodwill.

Conclusion

As time goes by is indispensable to be aware of environment of the company, and it means companies must adapt their strategies, to new trends and management tools.

The waste of time implies the losing of the company's position and the possible closing down. Quality costs analysis help the company in different ways such as, planning, development and control. This report shows the importance of how quality began, the most remarkable events throughout the history, and how they influenced the quality discipline, the procedures to calculate a particular quality cost, for “Stardust” and the main options to avoid quality costs.

In this case we estimate the turnover would be around £2M, since the quality cost amount is about £470k, it can be ascertained that we will have a great profit. Gradually with the implementation of the quality system, these costs will decrease and therefore profit will rise.

References and bibliography.

-Standards and quality management; an integrated approach.1995

-Margaret Cardwell.Customer care:strategy for the 90's.Quality management series.

-I.Graham.TQM in service industries.A practitioner's manual.

-R.H Caplen.A practical approach quality control.1972

-J.M Groocock.The Cost of Quality.1974

-Www.rincondelvago.com

- http://www.kaner.com/qualcost.htm

-Www.calidad.org

-Robson.Quality Circles;a practical guide.

-Quality circles;an executive guide.1992

-Dale B.Quality improvement through standards; 1994

-Bergman; Quality: from customers needs to customers' satisfaction.

Descargar

| Enviado por: | Froilan |

| Idioma: | inglés |

| País: | Reino Unido |

Todos los derechos reservados.