Historia

Unión monetaria de Europa

Introduction

The first of January 1999 (a few days ago) started the last stage towards the process of the European Monetary Union (EMU). Since that day, the national currencies of the EMU members are fixed at irrevocably exchange rate between one another (excluding the UK and Denmark, because the UK has maintained the right to opt out and Denmark subject to the agreement of a national referendum). From 1 July 2002 on, the euro will be the single currency of the EMU country members. This means that the devaluation/revaluation policy is not longer available for the countries that form the EMU (i.e. an EMU country can no longer change its exchange rate to correct for differential developments in demand or in costs and prices). The EMU country members have lost the ability to conduct a national monetary policy.

This dissertation looks first when a devaluation policy is used by countries and then, as the EMU countries have lost this instrument, the dissertation will look at alternative mechanisms to correct for differential developments in demand or in costs and prices.

The last part of the dissertation looks first to the costs and benefits of membership to the EMU countries and then it will look at the costs and benefits of membership to Spain

Chapter 1: Monetary Unions

1.1 What is a monetary union

We can define a monetary union (or area) as a geographic space in which the existing currencies in legal circulation exchange at a irrevocably fixed exchange rate. The final stage towards monetary union is a single currency area (later on, in this chapter, we will look at the three stages towards the European Monetary Union). A single currency area is one in which national currencies are effectively replaced by a unique single currency.

In a single currency area all the currencies would have to be exchanged for a unique currency. In this final stage the decision concerning the level of exchange rates (the conversion rates) that will be used to lock currencies irrevocably to each other will be taken.

1.2 Components of a monetary union

Let us now expose the components of the monetary union:

-

It has to be an area completely integrated monetarily, in which the exchange rates between the currencies of the countries that form it are irrevocably fixed between one another and fluctuate in a systematic way against the currencies of the rest of the world.

Although these two elements are already sufficient for the constitution of a monetary union, such an area will also be characterised by a common monetary policy and that makes equally necessary some elements of co-ordination of the economic policies between the country members. The conditions for establishing a monetary union are:

-

All the countries must allow the free circulation of capital in all the geographic area of the union without any restriction.

-

And, as we will see later on, it will not be possible to maintain the atmosphere of financial stability which is required to consolidate a project of this nature if it is not accompanied by certain institutional reform. Such reform must include, the design of the operative framework of the economic policies by which the countries will be governed. There will be one central bank, the European Central Bank (ECB), responsible for the monetary policy of the union as a whole. This central bank, therefore, will target union-wide variables, e.g. the total money stock in the union. In addition, the ECB will use the euro to implement these policies, e.g. it will buy and sell euros to influence the interest rate, or to target the money stock in the union.

1.3 Steps towards the monetary union

In order to achieve a monetary union, it is necessary to take some intermediate steps directed towards the regional integration that will gradually adopt a greater degree of co-operation. This is what has occurred in Europe over the last fifty years. So, the steps which have been taken over this period are:

The introduction of free trade, or an area of free trade, implies the disappearance of the tariffs between the signatory countries (of the agreement) and it also implies the maintenance of a common tariff against countries outside the monetary union. This characteristic indicates the main source of instability. If strong disparities exist with the tariffs against countries outside the monetary union, there will be a clear incentive for the trade to deviate towards the country that maintains an inferior level of protection, so that the product is re-exported towards other members of the free trade area if the transport costs do not prevent the profitability of the operation.

Let us now look at the second step. The custom union supposes, in addition to the elimination of the tariffs between members, the fixation of a common tariff against countries outside the monetary union. In this way the problem of incentives (previously mentioned) is eliminated, but the decisive question now is how to fix this common tariff. The discussion between more protectionistic and less protectionistic countries then become the key question. This explains, partially, the reluctance of the Nordic countries to join the initial group that signed the Treaty of Rome.

The common market adds to the customs union the free circulation of goods and factors of production. This last aspect is the one that has the most relevant results in the definition and where the major problems arise, mainly with the free circulation of capitals and its influence in the monetary and exchange policies of the countries. Such demands condition the cession of important elements in the exercise of the sovereignty by the member countries and explains the necessity for a clear political will in the attainment of this stage.

Such cessions of sovereignty are still more necessary and evident when it reaches the last stage in the regional integration. This is represented by the economic and monetary union. The objective of obtaining a unique currency demands the clear co-ordination of the macroeconomic policies of the different countries, otherwise the existence of a unique currency would be impossible. This would be incompatible with the excessive differences in the inflation rate or in the interest rates.

Description of the particular stages taken in Europe to achieve

monetary union

As we previously mentioned, we will now describe the particular stages taken to achieve monetary union in the European union.

In December 1991 the heads of state of the European Union signed a historic treaty in the Dutch city of Maastricht.

The Maastricht Treaty strategy for moving towards monetary union in Europe is based on two principles. First, the transition towards monetary union in Europe is seen as a gradual one, extending over a period of many years. Second, entry into the union is made conditional on satisfying convergence criteria.

The Treaty defines three stages in the process towards monetary union.

In the first stage (which had already started on 1 July 1990, prior to the signing of the Treaty), the European Monetary System (EMS) countries abolished all remaining capital controls. The degree of monetary co-operation among the EMS central banks was strengthened. During the first stage, which lasted until 31 December 1993, realignments remained possible.

The second stage started on 1 January 1994. A new institution, the European Monetary Institute (EMI), was created. It operates only during this second stage, and is in a sense the precursor of the European Central Bank (ECB). Its functions are limited, and are geared mainly towards strengthening monetary co-operation between national central banks.

The last stage started on 1 January 1999 (a few days ago). At the Summit Meeting of the heads of state in Madrid, December 1995, some agreements were made concerning the nature of the third stage. First, it was decided to call the new currency the euro. Second, the third stage was itself divided into three substages as follows:

-

From 1 January 1999 until 31 December 2001, the national currencies will continue to be in circulation alongside the euro, although at irrevocably fixed exchange rates. However, commercial banks will use the euro for all their interbank dealings. Private individuals will have the choice of using their national currency or opening an account in euros. Note that during this period the euro will not exist in the form of banknotes and coins. In addition, all transactions between the European Central Bank and the commercial banks will be in euros. Finally, new issues of government bonds will be made in euros and not in national currencies.

-

During the period 1 January to 1 July 2002 the euro will replace the national currencies, which will lose their legal-tender status. Thus, during this period a monetary reform will be organized.

-

From 1 July 2002 on, a true monetary union will come into existence in which the euro will be the single currency managed by one central bank, the European Central Bank (ECB).

Chapter 2: Optimum currency areas

An optimum currency area (OCA) is an economic unit composed of regions affected symmetrically by disturbances and between which labour and other factors of production flow freely (Mundell 1961).

As we previously mentioned, in the EMU from 1 January 1999 until 31 December 2001 the national currencies will be fixed at irrevocably exchange rates. During the period 1 January to 1 July 2002 the euro will replace the national currencies and from 1 July 2002 on, the euro will be the single currency. Therefore, the policy of devaluation or revaluation is no longer available for the countries that form the European Monetary Union (EMU). In other words, the constitution of the EMU implies that the joining countries relinquish the handling of the exchange rate and since they choose to integrate themselves in a voluntary way is reasonable to suppose that they do it for the advantages that it carries. Since the countries cannot change its exchange rate any more, the joining countries will now have to use alternative policies to correct for differential developments in demand, or in costs and prices.

2.1 The OCA theory

The OCA theory stresses the need to have labour market flexibility and labour mobility (these are alternative mechanisms to the devaluation/revaluations policies) as important requirements for a successful monetary union. This is because, countries or regions that experience a high divergence in output and employment growth need a lot of flexibility in their labour markets if they want to form a monetary union, and if they wish to avoid major adjustment problems. The OCA theory and the political economy analysis of the Maastricht Treaty also come out in favour of a small monetary union in Europe. The criteria to select the small group of countries, however, are different. In the OCA theory criteria such as wage flexibility, labour mobility and degree of economic integration stand out as the important ones for determining whether a country should be part of the union. According to the OCA theory, if the conditions of labour market flexibility and labour mobility are satisfied, there is no need to wait more than ten years to do it.

2.2 The exchange rate mechanism

The main cost associated when entering a monetary union is that the country relinquishes its national currency. In this way, it also relinquishes an instrument of economic policy, i.e. it loses the ability to conduct a national monetary policy. So, the cost of relinquishing one's national currency lies in the fact that a country can no longer change its exchange rate to correct for differential developments in demand or in costs and prices. This is what allow us to expose, in a more detailed way, the extent of the arguments in which the analysis relies upon the determination of the main cost associated with the constitution of a monetary area: the reduction of production and employment levels due to predictable negative demand shocks of an asymmetric nature. Not to have the faculty to vary the exchange rate implies that the country in question is more vulnerable during recession periods that can occur to its economy.

Let us use an example in order to see how the exchange rate mechanism works.

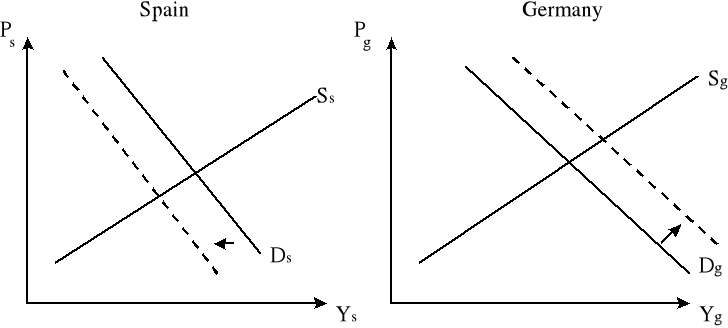

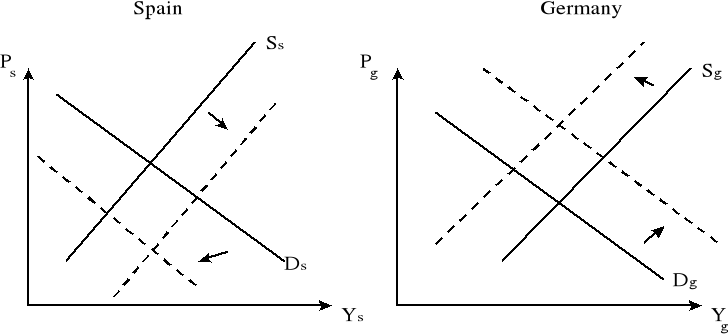

FIGURE 2.1: Aggregate demand and supply in Spain and Germany

Let us suppose that for some reason consumers shift their preferences away from Spanish-made to German-made product. We show the effects of this shift in aggregate demand in Figure 2.1.

The curves in Figure 2.1 are the standard aggregate demand and supply curves in an open economy. The demand curve is the negatively sloped line indicating that when the domestic price level increases the demand for the domestic output declines.

The supply curve expresses the idea that when the price of the domestic output increases, domestic firms will increase their supply, to profit from the higher prices. These supply curves therefore assume competition in the output markets. In addition, each supply curve is drawn under the assumption that the nominal wage rate and the price of other inputs remain constant.

The demand shift is represented by an upward movement of the demand curve in Germany, and a downward movement in Spain. The result is that output declines in Spain and that it increased in Germany (see figure 2.1). This is most likely to lead to additional unemployment in Spain and a decline of unemployment in Germany. Therefore, the direct effects of this asymmetric shock would be: a decrease in output and prices in Spain and an increase of prices and output in Germany (see figure 2.1). The problem would be that in Spain domestic output and employment will be reduced. Whereas, in Germany there is an inflationary process due to the excess demand caused by the arrival to its market of consumers coming from the other country, where the aggregate demand has been reduced.

Now we will contrast the position where both countries have a separate currency (and therefore can devalue their currencies) with the position where both countries are part of a Monetary Union.

Due to the existence of mechanisms in the economies of these two countries, that lead to automatic equilibrium, the internal cost will not vary in the same quantity in both countries. Thus the increase in the demand of products in Germany and the corresponding decrease in the demand of products in Spain, will generate a current account surplus in Germany and a current account deficit (of equal magnitude) in Spain.

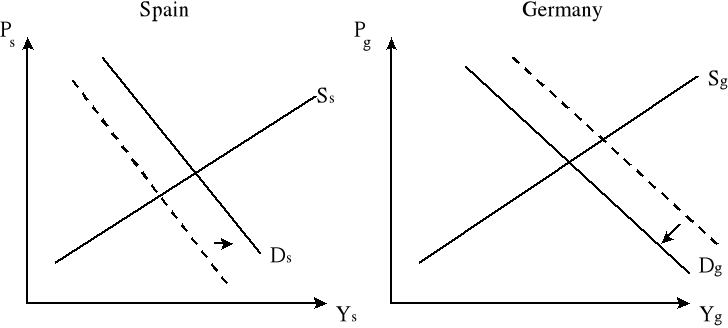

Spain can solve the problem previously mentioned (that consumers shift their preferences away from Spanish-made to German-made products) devaluing the peseta against the mark. The effects of this exchange rate adjustment are shown in Figure 2.2 (see next page):

FIGURE 2.2: Effects of a devaluation of the peseta

The devaluation of the peseta increases the competitiveness of the Spanish products, this shifts the Spanish aggregate demand upwards. In Germany the opposite occurs. The revaluation of the mark (against the peseta) reduces aggregate demand in Germany, so that the demand curve shifts back to the left (see figure 2.2).

The effects of these demand shifts is that Spain solves its unemployment problem, and that Germany avoids having to accept inflationary pressures. At the same time, the current account deficit of Spain and surplus of Germany tend to disappear.

Now we will contrast this situation with the situation where Spain and Germany form a Monetary Union. If Spain has relinquished the control over its exchange rate by joining a monetary union with Germany, it will be saddled with a sustained unemployment problem, and a current account deficit that can only disappear by deflation in Spain. In this sense we can say that a monetary union has a cost for Spain when it is faced with a negative demand shock. Similarly, Germany will find it costly to be in a monetary union with Spain, because it will have to accept more inflation than it would like.

As we can see, the flexibility of the exchange rate can recover the initial equilibrium with no need for intervention in the economy. This is essentially a `keynesian' view based on the ideas that the world is full of rigidities (wages and prices are rigid, labour is immobile), so that the exchange rate is a powerful instrument for eliminating desequilibria. However the alternative view is that devaluation can have little if any effect in either the long-run or short-run. This alternative view which emphasises considerations of reputation, credibility in response to market expectations is explained in detail below.

On this view, the irrevocable fixation of the exchange rates (that brings the formation of a monetary union) prevents the national authorities use of this natural adjustment mechanism. It also forces the national authorities to adopt alternative mechanisms that, while they correct the exterior disequilibrium, they cause certain induced effects on economic magnitudes of internal character.

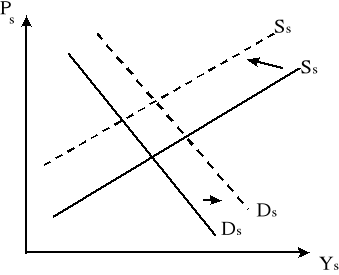

Let us take the case of Spain developed earlier. We assumed that a shift occurred from Spanish products in favour of German products. In order to cope with this problem Spain devalues its currency. We present the situation in Figure 2.3 below.

FIGURE 2.3: Price and cost effects of a devaluation

As a result of the devaluation, aggregate demand in Spain shifts back upwards and corrects for the initial unfavourable demand shift. The new equilibrium point is F (see figure 2.3).

It is unlikely that this new equilibrium point can be sustained. The reason is that the devaluation raises the price of imported goods. This raises the cost of production directly. It also will increase the nominal wage level in Spain as workers are likely to be compensated for the loss of purchasing power. All this means that the aggregate supply curve will shift upwards. Therefore, prices increase and output declines. These price increases feed back again into the wage-formation process and lead to further upward movements of the aggregate supply curve. The final equilibrium will be located at a point like F'(see figure 2.3). The initial favourable effects of the devaluation tend to disappear over time

From this last example we can say that the devaluation of a national currency will initially bring favourable effects. The devaluation raises the price of imported goods, this raises the cost of production directly and it also will increase the nominal wage level of the country as workers are likely to be compensated for the loss of purchasing power. As a result, prices increase and output declines in the country that devalues its currency. But these initial favourable effects of the devaluation tend to disappear over time. What we cannot say is whether these favourable effects of the devaluation on output will disappear completely. This depends on the openness of the economy, on the degree to which wage-earners will adjust their wage claims to correct for the loss of purchasing power. In other words, nominal devaluations only lead to temporary real devaluations. In the long run nominal exchange rate changes do not affect the real exchange rate of a country. So, we can say that exchange rate changes are ineffective in the long run, but this does not imply that countries do not lose anything by relinquishing this instrument (the exchange rate). We also have to analyse the short-term effects of an exchange rate policy, and we have to compare these to alternative policies that will have to be followed in the absence of a devaluation.

An alternative policy can be an expenditure-reducing policy. In general expenditure reducing policies reduce domestic demand for the domestic good. These expenditure-reducing policies, also reduce aggregate demand for the domestic goods. We can say that in the long-run the two policies (devaluation and expenditure-reducing) lead to the same effect on output and the trade account. In other words, in the long-run the exchange rate will not solve problems that arise from differences between countries that originate in the goods markets. This result is also in the tradition of the classical economists.

The difference between the two policies, a devaluation or an expenditure-reducing policy, is to be found in their short-term dynamics. When the country devalues, it avoids the severe deflationary effects on domestic output during the transition. The cost of this policy is that there will be inflation. With the second policy, inflation is avoided. The cost, however, is that output declines during the transition period. In addition, this second policy may take a long time to be successful if the degree of wage and price flexibility is limited. We can conclude that although a devaluation does not have a permanent effect on competitiveness and output, its dynamics will be quite different from the dynamics engendered by the alternative policy which will necessarily have to be followed if the country has relinquished control over its national currency. This loss of a policy instrument will be a cost of the monetary union. There is a lot of empirical evidence that a devaluation will help to restore domestic and trade account equilibrium at a cost that was most probably lower than if it had not used the exchange rate instrument (e.g. Belgium in 1982, French devaluation of 1982-3, Danish devaluation of 1982).

Criticism of the devaluation policy

Let us now come back to look at the arguments that devaluation can have little or no effect in either the long-run or the short-run.

Policies of inflation and devaluation of the currency have only temporary effects on output and employment. In the long-run, inflation and depreciation of the currency have no or only limited effects on these variables. In the monetarist models of the world (e.g. vertical long-run Phillips curve, or a vertical long-run aggregate supply curve) inflation and depreciations of the currency have no effects on output and employment. As a result, in this monetarist world the cost of a monetary union (which is associated with the loss of the power to devalue) is really zero.

Let us now criticize the view that the exchange rate is a policy tool that governments have at their disposal to be used in a discretionary way.

Pegged exchange rate systems face some important problems that have led many economists to doubt the long-run sustainability of these systems. A first problem has to do with the credibility of the fixed exchange rates. A second one concerns the way the system-wide monetary policy is determined. Lets see each one in turn:

The credibility problem arises for two different reasons. The first reason is that the use of the exchange rate can sometimes be the least-cost instrument to adjust the economy after some disturbances. The second reason follows from the Barro-Gordon analysis (Barro, R. and Gordon, D. 1983) stressing that governments have different reputations, which may undermine the credibility of a fixed exchange rate. Let us analyse these two problems consecutively.

Adjustment problems lower the credibility of a fixed exchange rate. When two or more countries decide to peg their exchange rates, economic agents realise that there may be future situations in which a change in the exchange rate would minimise adjustment costs. They therefore also know that when these future situations occur, the authorities will have an incentive to renege on their commitment to keep the exchange rate fixed. As a result, such a fixed exchange rate commitment will have a low credibility, and will often be subjected to speculative crises. This credibility problem can be solved only if the authorities convince speculators that their only objective is the maintenance of the fixity of the exchange rate, whatever the output and employment costs.

Differences in reputation lead to low credibility of a fixed exchange rate. Once the exchange rate is fixed, it has an incentive to follow inflationary policies and to devalue by surprise, so as, to obtain a more favourable inflation-unemployment outcome. This, however, will be anticipated by economic agents, who will adjust their expectation of inflation. This will force the authorities to devalue the currency regularly. In addition, the regular devaluations will be anticipated, leading to large-scale speculative crisis prior to the anticipated dates of realignments. The fixed exchange rate commitment will collapse. Let us illustrate this by the following example (see next page).

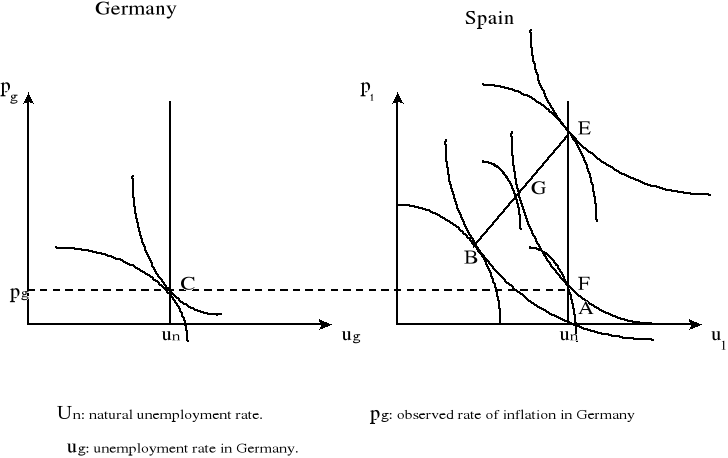

FIGURE 2.4: Inflation equilibrium in a two-country model

Let us assume that only unexpected inflation affects the unemployment rate, we will also use the rational expectations assumption. Suppose also that there are two countries, we call the first country Germany and assume that its government is `hard-nosed' (`hard-nosed' monetary authorities are willing to let the unemployment rate increase a lot in order to reduce the inflation rate by one percentage point). The second country is called Spain, where the government is `wet' (`wet' governments are willing to accept a lot of additional inflation in order to reduce the rate of unemployment by one percentage point).

Suppose, now, that Spain announces that it will fix its exchange rate with the German mark. Given the purchasing-power parity, this fixes the Spanish inflation rate at the German level. In Figure 2.4 we show this by the horizontal line from C. Spain appears now to be able to enjoy a lower inflation rate. The potential welfare gains are large, because in the new equilibrium the economy is on a lower indifference curve.

The question, however, is whether this rule can be credible. We observe that once at the new equilibriun point F, the Spanish authorities have an incentive to engineer a surprise devaluation of the peseta. This surprise devaluation leads to a surprise increase in inflation and allows the economy to move towards point G. Over time, however, economic agents will adjust their expectations, so that the equilibrium inflation rate ends up to be the same as before the exchange rate was fixed. Thus, merely fixing the exchange rate does not solve the problem, because the fixed exchange rate rule is more credible than a fixed inflation rate rule.

This analysis lead to the conclusion that the high-inflation country (Spain) has a lot to gain from pegging its currency to the currency of a low inflation country. However, Spain will find difficult to fix its exchange rate credibly.

The liquidity problem in pegged exchange rate systems. Every system of fixed exchange rates faces the problem of how to set the system-wide level of the money stock and interest rate.

The time-consistency literature also teaches us some important lessons concerning the costs of a monetary union: a devaluation cannot be used to correct every disturbance that occurs in an economy. A devaluation is not, a flexible instrument that can be used frequently. When used once, it affects its use in the future, because it engenders strong expectations effects. It is a dangerous instrument that can hurt those who use it. Each time the policy-makers use this instrument, they will have to evaluate the advantages obtained today against the cost, i.e. that it will be more difficult to use this instrument effectively in the future.

This has led some economists to conclude that the exchange rate instrument should not be used at all, and that countries would even gain from irrevocably relinquishing its use. This conclusion goes too far. As we previously mentioned, there were many cases, observed in Europe during the 1980s, in which devaluations were used very successfully. The reason of this success have typically been that the devaluation was coupled with other drastic policy.

Note that the movement towards a common currency will eliminate the exchange risk, and therefore will lead to a more efficient working of the price mechanism.

2.4 Conditions for an optimal monetary union

. There are many works (Mundell, Kenen, McKinnon) that have come to show that the adjustment mechanism (that causes the exchange rate) can also be obtained in other ways with no need to have to resort to the procedure (in many cases painful for certain agents) that supposes the control of the aggregate demand by policies that reduce expenses. These authors identify the conditions necessary for a country to relinquish its currency and therefore the power to devalue (They wrote that the countries are able to do so because other instruments are available or because the economy is sufficiently flexible). But when Mundell, Kenen and McKinnon wrote the arguments about the limits to devaluation were less well developed than they are now. These analyses put, at the same time, a clear idea about the conditions that are to be fulfilled so that the constitution of a monetary union is optimal. These works show that is not specially important the fact of being able to control the mechanism of the exchange rate. This is because the monetary union between several countries would be optimal whenever these conditions are fulfilled:

-

Flexibility in the fixation of wages (wage flexibility);

A perfectly flexible labour market is one in which if there is an increase of unemployment in a country, the workers would accept to work at a lower wage. In this way entrepreneurs would increase the demand for work and this new-equilibrium would leave as a consequence the return to the initial situation in the level of production. In addition to this, the decrease of prices in this country would benefit the relation of exchange, increasing the purchase of products of this country. In this way, the initial position of the aggregate demand would be recovered and the deficit of the country would be eliminated. On the other hand, in the other country the opposite would happen: the excess demand of labour would increase wages, causing an increase in prices and with it a decrease in the demand of products in this country. In this way, the current account surplus of this country would be reduced.

Lets consider that for some reason EU consumers shift their preferences from Spanish-made to German-made products. If wages in Spain and Germany are flexible the following will happen. Spanish workers who are unemployed would reduce their wage claims. In Germany the excess demand for labour will push up the wage rate. In Spain the price of output declines, making Spanish products more competitive, and stimulating demand. The opposite occurs in Germany. This adjustment at the same time improves the Spanish current account and reduces the German current account surplus. We can see this effects by looking figure 2.5 (see next page):

Figure 2.5The automatic adjustment due to wage flexibility:

-

High mobility of labour in all the territories of the union

In this case, the excess demand of labour in a country would imply that the unemployed people of other countries will move to the country with greater demand of labour. This movement of labour eliminates the need to let wages to decline in the country with unemployment and increase in the country with little demand of labour. Thus, one country would eliminate its unemployment problem and in the other country the inflationary wage pressures vanish. It has to be said that the production and expenses will be again in equilibrium in both countries because in the country with smaller production, it no longer has to pay subsidies of unemployment. In this way, eliminating the imbalance in its balance of payments.

-

The framework of the economic relations

Other studies have shown how the supposed advantage of the flexible exchange rate to reach non-traumatic adjustments compared to the fixed exchange rate (demanded by the monetary union) can only be obtained under certain conditions.

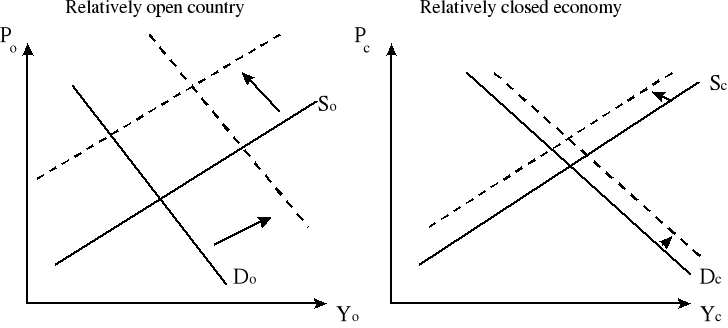

In 1963 McKinnon demonstrated that that advantage is only possible in cases of economies very closed to the exterior competition, in which a devaluation of the currency to fight the loss of competitiveness can only obtain its objective when the country has little dependency on the exterior. There are several views that bear on the question of how the openness of a country affects the cost of the monetary union. We will concentrate on two (European Commission versus Krugman view). These views have opposite effects. First, there is the relation between the degree of openness (the degree to which a country is integrated with the rest of the world) and the occurrence of asymmetric shocks. The European Commission view sees a negative relationship between the cost of monetary union and the openness of countries. According to this view, the more openness reduces the cost of a monetary union, as it reduces the probability that asymmetric shocks occur. This matters because if there are asymmetric shocks we need country specific policy tools (perhaps devaluation), if they are not country specific then it is an European Union (EU) problem.

The Krugman view sees a negative relationship between the cost of monetary union and the openness of countries. According to this view, the costs of a monetary union increase with the degree of openness of countries. How the openness affects the cost of monetary union has to do with the effectiveness of the exchange rate in dealing with asymmetric shocks. Let us return to Figure 2.3, where we analysed the effects of a devaluation. We now consider two countries, one relatively open, the other relatively closed. We present these two countries in Figure 2.6 below.

FIGURE 2.6: Effectiveness of devaluation as a function of openness

Both the demand and supply effects of a devaluation differ between the two countries. As far as the demand-side effects are concerned, the same devaluation has a stronger effect in the relatively open economy than in the relatively closed one. In Figure 2.6 we show this difference by the fact that the demand curve in the relatively open country shifts further outward than in the relatively closed country.

The two countries also differ with respect to the supply-side effects of the devaluation. One can expect that in the relatively open economy, the upward shift of the supply curve following the devaluation is more pronounced than in the relatively closed economy

So, a devaluation will be felt more strongly on the aggregate price level in the more open economy than in the relatively closed economy. This means that the systematic use of the exchange rate instrument will lead to more price variability in the more open economy than in the relatively closed one. To the extent that price variability involves costs, the systematic use of the exchange rate instrument in the more open economy will be more costly. This point was first recognised by Mckinnon (1963).

We can conclude that for the same effect on output, the devaluation is likely to be more costly in the open economy because of the higher price variability involved. Therefore the loss of the exchange rate instrument is likely to be less costly for the relatively open economy than for the relatively closed one. So, the cost of monetary union most likely declines with the degree of openness of a country.

Combining the analysis of the effectiveness of a devaluation with the analysis of the relationship between openness and asymmetric shocks, we can conclude that the cost of monetary union most likely declines with the degree of openness of a country. We show this in Figure 2.7:

FIGURE 2.7: The cost of a monetary union and the openness of a country.

Cost (%GDP)

Trade (%GDP)

On the vertical axis is set out the cost of a monetary union (i.e. the cost of relinquishing the exchange rate instrument). This cost is expressed as a per cent of GDP. On the horizontal axis is set out the openness of the country relative to the countries with whom it wants to form a monetary. We see that as the openness increases the cost of joining a monetary union declines.

Later on (in 1969), Kenen considered the assumption of diversification. Kenen postulated that the exchange rate adjustments would not be necessary in those economies in which the incidence of a decrease in the demand for a concrete product had on the general conditions of that economy, was not important. In order for this to happen a high degree of diversification in its production activity would be enough. In this sense, we can affirm that the greater the degree of diversification of the productive activity (in the countries that comprise the union) the more advantageous the union.

With analogous reasoning (in 1973) Magnifico and Ingram demonstrated that one benefit for the formation of monetary unions will be that the exterior relation framework between the countries is developed in surroundings of concrete structural conditions. According to Ingram, if the countries had a high degree of financial integration, the capital movements would compensate the disequilibrium with no need to resort in the variation of the exchange rate. For Magnifico, it is advisable that the inflation levels are similar between the countries that are arranged to form the monetary union. In this way, the necessity to have to modify the exchange rate to compensate the loss in competitiveness would be eliminated.

-

The degree of budgetary concentration

If we leave to one side the movements of the variables, such as production, employment or prices and we pay attention to the level of domestic output available. We can see that in situations where a concrete area of the union suffers a period of recession, this period could be mitigated to a large extent (without existing wage flexibility or high mobility of labour) thanks to the transfers of output between the countries. In fact, this is the correction mechanism of the territorial disequilibriums within areas perfectly integrated monetarily, as they can be the regions of a country. Thus, when a region undergoes a period of recession that does not affect in a similar way to the rest of the areas in the same territory, which is monetarily integrated in a perfect form. The central administration corrects (or at least tries to correct) by output transference's from the prosperous areas to areas in a recessive period. This is achieved when less taxes are paid and when more expenses are received.

This is only possible if the authorities of the monetary union had a general budget that could fulfil the compensatory function in an automatic way, this demands a great budgetary centralisation. If this occurred, it would be by itself the sufficient and necessary condition so that a monetary union could be considered an optimum currency area.

CHAPTER 3: Costs and Benefits of becoming a member of

the EMU

The evaluation of the policies of economic integration demands an indication of the benefits and costs produced in the process. From our first chapter we should remember that such effects take place as a result of three processes that started an agreement of economic integration. These three processes are known as: trade creation, trade divesion and trade expansion.

The first process refers to the substitution of national products by imported products, these imported products coming from the member countries of the integration agreement and from countries outside the integration agreement. There are products coming from the member countries due to the disappearance of the tariff between the signatory countries of the agreement, and there are products coming from other countries due to the reduction in the pre-existing tariff against the countries outside the monetary union. The second process indicates the substitution of an imported product by a product coming from the exterior. This process occurs due to the disappearance of the tariff between the country members that make its products more competitive than the products coming from the countries outside the union (to these products they continue applying a tariff). Finally, the expansion of the trade is generated in the long run, when the advantages that the trade integration proposed end up showing inferior prices. Such reduction in prices makes more competitive, in the exportation, the national products.

3.1 The benefits of membership

The expected benefits from a monetary union are associated mainly with the economies of scale, obtained from the elimination of the national currencies and their substitution by a common currency. These benefits can be evaluated in economic efficiency terms. The prevailing theory shows that the monetary efficiency gains, which can be obtained with the implantation of a union of this nature, are basically three:

-

Monetary discipline and economic credibility; the countries that constitute a monetary union relinquish the independent handling of the monetary policy since the monetary policy will be now controlled by the central bank created for the union. In this way, the countries loose the possibility of using this internal control instrument of the national economic activity. Now the national economic activity will have to be regulated by the other two alternative mechanisms: the fiscal policy and the incomes policy. This is a positive thing because it introduces a powerful factor of internal discipline since a form of avoiding the adjustments entails the use of these mechanism of control. This faithfully fulfils the rules imposed by the authorities of the union. With it, on the other hand, a greater degree of credibility is installed to the national and foreign agents about the long term maintenance of the country's economy stability conditions. Naturally, these favourable effects will be greater in those countries that before the constitution of the monetary union offered smaller guarantees of credibility, since these countries move on to participate in the credibility that the monetary union grants in a general way.

The European System of Central Banks (ESCB) would provide a strong anchor for price stability, and generally give the entire system a greater degree of credibility for its monetary stance.

If such a price stability anchor were achieved, with reduced nominal exchange rate uncertainty, then interest rates would be expected to be lower for a number of reasons. Firstly, nominal interest rates would decline by the same amount as inflation, even with constant real interest rates. Secondly, the experience of countries such as the Netherlands and France has shown that real interest rates have to be higher when there is uncertainty about inflation. With price stability this will not be necessary. Thirdly, real interest rates could be lower before an induced fall in inflation in the EMU, even in those countries in which inflation is least under control.

-

The elimination of the transaction costs; one of the main advantages of the European Monetary Union is the removal of transaction costs between currencies. A single currency would eliminate the present costs of converting one EC currency into another. This would give an estimated savings of 15 billion ECU or 0.4% of GDP. These gains come from the disappearance of Bank transaction costs. Transaction costs vary, depending on the country and method used. It seems that individual small transactions would benefit the most, and therefore small and medium sized companies and tourists would benefit. This in turn would encourage exports, which would be internalised.

Apart from the exchange transaction costs being eliminated by a single currency there would also be an important cut in the present expenses and delays associated with cross-border bank payments. There will be a great reduction in the complexity of banks' treasury management, accounting and reporting to monetary authorities. International bank transfers and cross-border payments will become as quick and inexpensive as domestic ones made today.

-

Smaller uncertainty in the evolution of the exchange rates; an attributable disadvantage to the use of flexible exchange rates is that using them increase the economic agents insecurity when they have to make decisions. This is because there will be a greater uncertainty about the future exchange relations. On the other hand, the establishment of a fixed exchange rate (consubstantial element in the constitutions of monetary unions) eliminates the risk of uncertainty in the transactions with the exterior. The establishment of fixed exchange rates can also constitute a determining factor in the fomentation of those relations, especially in those relations where the economic results are more unpredictable (for example, relations destined to investment). Definitively, the elimination of uncertainty in the exchange rate evolution increases the degree of information of the economic agents at the time of taking decisions on production, consumption and investment. As well as eliminating factors of risk in growth models, it will provide an increase in the well-being of the society.

Therefore, the elimination of exchange rate movement would reduce uncertainty about fluctuation in nominal exchange rates and thus should stimulate trade and investment. As a result, low-wage regions could well benefit the most. The gains in terms of increased trade and capital movements are difficult to measure as firms often insure against the risk of exchange rate variation by the use of sophisticated foreign exchange market operations.

-

Advantages derived from regional integration; a first argument in favour of the total integration is the reallocation of private industries by considerations of economic efficiency. The traditional idea is that the industries are located by looking at low production costs and wide markets for its products. Then, the argument is based on the idea that the integration reduces the costs associated with the transport of goods from one territory to the other. And in this way, accentuates the attraction for the countries with lower costs; nevertheless in order for this advantage to be total, an efficient network of infrastructure and communications is necessary. The second relevant element is based on the pro-competitive effect that generates the integration. The presence of natural monopolies is justified by the size of the market therefor, they have no need for bigger markets. Now then, the transformation process and the loss of this monopolistic position have important costs of adjustment that can be lowered if they are suitably planned. Thirdly, it is adduced that the reduction of the trade costs will make the presence of foreign companies in our country possible, replacing the less efficient national companies and thus favouring the consumers.

-

Comparison of international prices (price transparency); assuming that the markets are perfectly integrated, it will be easier to compare the prices of the countries in a common currency. This will incise to a process of price reduction, in order to make prices more competitive compared to the rest of the economies.

Static and dynamic gains would be enhanced through the encouragement of competition and price transparency. Fixed investment between countries would be stimulated as business decisions would be unaffected by currency uncertainties.

It is generally agreed that a single market will bring large benefits, however most standard theories of economic growth incorporate constant returns to scale and perfect competition and do not allow for integration to affect growth in the long run.

When the internal market is completed people, goods, services and capital will move freely. The expected economic impact of this was estimated in the Cecchini Report; in which welfare gains of between 2.5 and 6.5 percent of the Community GDP were found through a microeconomic approach. When translated through macroeconomic simulations this showed a medium-term increase in GDP of 4.5 percent, a 6 percent fall in the price level, and a 1.5 percent rise in employment, i.e. almost 2,000,000 jobs. Additional research has been undertaken since this report, looking at the dynamic effects not covered by Cecchini and these further benefits have been shown to be substantial.

3.2 The costs of membership

Without doubt the more sensitive and immediate consequences (that supposes for any country the entrance to a monetary area of this nature) are the loss of the protective properties (by the authorities of that country) that entails the possibility of variation of the exchange rate in the economic relationship with the exterior.

The exchange relation of goods between countries with different currencies depends on these two factors: the price at which the goods are sold in both countries and the exchange rate between the two currencies. In this way, given certain relative prices between these two currencies, the exchange rate between these two countries (in other words, the proportion by which one currency can be exchanged by the other) is what determines the exchange relations among them. This allow us to appreciate the fundamental role that has for the authorities of each country to maintain the control of the possibility of variation of the exchange rates. If for example, one of those two countries is affected by an inflation process, this will make worse its exchange relation with a country in which the prices have stayed stable. One way of recovering the competitiveness with this country, without adopting anti-inflationary measures, is to act on the other determining factor of the situation: the exchange rate. The exchange relation between countries can be recovered with a devaluation of the national currency.

It is for this reason, why the relinquish to the independent handling of this instrument of control means in fact that the authorities of the countries in question are forced to defend the competitiveness of the economy through measures that allow the control of prices (the really guilty variable of the deterioration of the exchange relation). But in addition, we do not only lose an instrument of adjustment, we also renounce to recover the exchange relation through the natural mechanism in the international trade: the exchange rate. Now, the authorities will be forced to do it through mechanisms that cause direct effects on variables of internal order, such as the level of prices. It is for this reason why the constitution of monetary unions have an inevitable cost: the voluntary relinquish to the independent handling of the exchange rate. Monetary policy would no longer be able to be used for demand management and domestic economic control. Interest rates could not be set to levels appropriate for the control of domestic demand. However this is as much a benefit as a cost. An open economy with free capital flows does not have much influence over real interest rates anyway.

Devaluation will no longer be available as an instrument for correcting a loss of competitiveness in Spain relative to its European partners. In the long run this should not be important since real market forces would work to restore appropriate relative prices. It seems a reasonable assumption that monetary institutions, in the long run are unable to influence the underlying real economy in the sense that relative prices cannot be set by monetary policy. Although it must be noted that sustained inflation can result in permanent output loss.

Loss of national monetary policy also may not matter if the countries of the EC are asymmetrical and highly integrated industrially. If this is the case then each country becomes a microcosm of the larger whole and so an optimal policy response to a shock in one country should also be optimal for the Community as a whole.

Another main disadvantage is the potential loss of sovereignty. Economic theory argues that the loss of independent national monetary authority only matters to the extent that such monetary policies have real effects. In a perfect market, monetary changes would have a direct effect on prices without affecting any real variable such as unemployment. Therefore, in such a world, when a country's monetary authority loses power to change the rate of growth of money, it is only losing the power to affect the subsequent inflation rate, rather than altering anything real. The importance of the loss of national monetary authority depends, therefore, on how close the EC market is to a perfect market, as this will determine the extent to which monetary policies do have real effects.

National monetary authorities will lose the ability to issue monetary liabilities with the adoption of a single currency. Hence seigniorage benefits will be lost by a high inflation country joining a low inflation EMU.

Since most countries have now reduced their inflation rates the loss of seigniorage benefits will be small and insignificant compared with the benefits.

If we assume a perfect labour mobility, a problem related to the wage differences can arise. The employees of the country with smaller wages will have an incentive to request the same wage as the employees in the country with higher wages. If this happens, it will cause an increase in the price levels in the country in which initially smaller wages were paid. This is because we would be in a situation where prices could be very easily compared between countries, due to the implantation of a common currency in all the country members.

.

Chapter 4: Costs and Benefits of membership to Spain

The evaluation of costs and benefits that the Monetary Union offers to Spain is a complex exercise, this is because we have to consider many factors and because these factors are interrelated. In this chapter we will try to show what the European Monetary Union (EMU) can offer to Spain.

The three main direct consequences of the EMU to Spain are: the country loses the ability to conduct a national monetary policy, the fiscal policy instruments limitation and the qualitative and irreversible change in the economic integration process with Europe. But the EMU offers, primarily, a formidable challenge and a great opportunity for Spain.

The fiscal policy limitation and the loss of the ability to conduct a national monetary policy implies a cost. This cost lies in a greater difficulty to stabilise the economy against asymmetric disturbances.

Let us now see what made inevitable the devaluation of the peseta in September 1992.

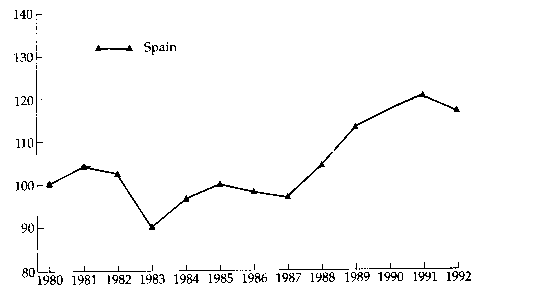

FIGURE 4.1: Price index in Spain relative to Germany (expressed in common currency).

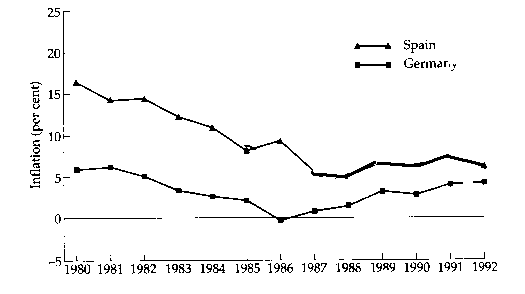

FIGURE 4.2: Inflation rates of Spain and Germany.

At the start of the 1990s the EMS had evolved into a truly fixed exchange rate system with (almost) perfect capital mobility. In this new monetary environment, the credibility and the liquidity problems started to have their full destabilizing effects. One problem arose mainly in connection with the peseta. Despite vigorous and in a sense successful efforts at reducing inflation in Spain, Spain did not manage to close the inflation gap with Germany. This certainly had something to do with differences in the reputation of the monetary authorities in Spain versus Germany which made it difficult to reduce inflationary expectations in Spain to the German level. As a result, actual inflation rates in Spain failed to move to the German level. Since the early 1980s the inflation rate of Spain converged on the German one without, however, moving towards equality with it (we show empirical evidence in figure 4.2).

This situation led to a credibility problem. Spanish inflation rate remained above the German one for many years, the price level of Spain tended to diverge continuously from the German one. Since there were no realignments after 1987 to compensate for these divergent price trends, a continuous loss of competitiveness of the Spanish industry occurred.

During the 1980s Spanish prices increased by close to 20% relative to German prices (see figure 4.1). This divergent trend in price levels jeopardized the competitiveness of the Spanish industry. At the end this became unsustainable, this made the devaluation of the peseta in September 1992 inevitable. This suggests that a slow transition process, which makes the steps towards the final stage of monetary union conditional on the existence of full convergence of inflation rates, is a dangerous one for Spain.

Now we will come back to analyse the cost that implies the fiscal policy limitation and the loss of the ability to conduct a national monetary policy. The relevance of this cost is explained when the following aspects are taken into consideration:

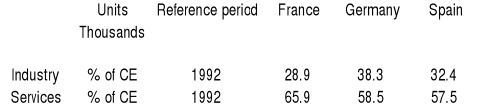

Firstly, it is not expected that the asymmetric disturbances will be very relevant throughout Europe. The differential demand disturbances will be drastically reduced inside the EMU, since these disturbances have been originated by the use of a undisciplined fiscal policy in the past. On the other hand, the similarity of the productive structures make the existence of asymmetric disturbances related to the productive structure less likely. Let us see the similarity of the Spanish, France and German productive structure by looking at the table below:

TABLE 4.1: Industry and Services productive structure in France, Germany and Spain.

Source: OECD Economic Surveys (Spain 1996).

From the above table we can see that the productive structures of France, Germany and Spain are quite similar.

Secondly, it is doubtful that the exchange rate can be used as an instrument of stabilisation against real disturbances. Firstly, the exchange rate has responded mainly to monetary disturbances more than to real disturbances, which in theory are the ones' it should have stabilised. Secondly, on the other hand, in the last decade the Spanish peseta has been submitted to a partially-fixed system, this is why its handling in a discretionary way has been limited. Thirdly, in a high financial integration context, it is illusory to think that a country can manipulate its exchange rate in a discretionary way. This is because the country is conditioned by the financial markets. Finally, the devaluations that the Spanish peseta has suffered in previous years has been used to correct disequilibriums generated mainly by the monetary divergences or to eliminate the speculative pressures of the financial markets. This is shown in the inevitable peseta devaluation in 1992 previously mentioned.

But we should not arrive to the conclusion that the disappearance of the exchange rate and the loss of the fiscal autonomy are innocuous in the actual circumstances. The rigidities that affect prices and wages formation mechanisms in Spain, could generate (if they persist) inflation differentials and loss of competitiveness.

In any case, the potential solutions that the EMU discards (the manipulation of the exchange rate or fiscal expansions above the limits set up in the stability agreement) are not optimal. The main problem relates to the structural characteristics of the economy, that can make the accomplishment of the necessary adjustments to the new environment with greater outer competition difficult.

The unequivocal benefit of the monetary union is that it will help to restore a situation (framework) of greater macroeconomic stability.

This affirmation is based on the following considerations: firstly, the disappearance of the exchange will entail, simultaneously, the disappearance of the monetary divergences and the speculative movements upon the peseta; both are important sources of instability; secondly, the EMU has been conceived as an area of monetary stability, which will result in a lower level of inflation for Spain; thirdly, the stability agreement that accompanies the monetary union supposes a greater budgetary discipline.

All these elements imply a framework with greater macroeconomic stability, which will allow Spain to increase its growth capacity because it will favour the processes of capital accumulation. In the case of Spain, it is also necessary to emphasise that a greater stability must contribute to moderate the disequilibriums that traditionally have accompanied the economic expansion periods. Since these disequilibriums have prevented the continuity of the expansions, it is to hope that the EMU will facilitate the road to a more sustainable growth in the long-run.

As we previously said, Spain will gain a lower level of inflation by becoming a member of the European Monetary Union. But as a result Spain will have to increase taxes, thus there will be a loss of welfare. Why? In general, countries with an underdeveloped tax system will find it more advantageous to raise revenue by inflation (seigniorage). In other words, a country with underdeveloped fiscal system experiences large costs in raising revenue by increasing tax rates. It will be less costly to increase government revenue by inflation. This reasoning leads to the following implication for the costs of a monetary union. Less developed countries that join a monetary union with more developed countries that have a low rate of inflation will also have to lower inflation. This means that, for a given level of spending, they will have to increase taxes. There will be a lose of welfare. Some economists have claimed that this is a particularly serious problem for the southern EC countries (this is the case of Spain). By joining the low-inflation northern monetary zone they will have to increase taxes, or let the deficit increase further. So for Spain one cost of the monetary union is that it will have to rely too much on a costly way of raising revenues.

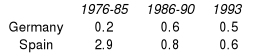

TABLE 4.2: Seigniorage revenues as per cent of GNP

Source: De Grawe (1997).

Table 4.2 gives some empirical evidence on the size of the seigniorage for Spain and compares it with Germany. We observed that up to the middle of the 1980s Spain had high seigniorage revenues. However, since the middle of the 1980s seigniorage revenue has declined significantly, mainly because of the reduction in their inflation rates. This leads to the conclusion that if Spain joins the Monetary Union with low-inflation countries, the additional cost (in terms of public finance) would probably not be very important for Spain.

The challenge of the monetary union consits in improving the capacity of adaptation and the flexibility of the economy so that the integration becomes more beneficial and, therefore, confirms the good expectations created around it.

The transcendence of the monetary union is the transition of a European context in which different economic systems have been able to survive, protected under a wide set of economic policy instruments, to a regime in which (beyond the competition between markets) a true competition between economic systems will be verified. The most prepared systems or the ones' that will adapt better to the new regime will be the greatest beneficiaries of the Monetary Union.

The Spanish economy could have a considerable decrease in the advantages that, potentially, are derived from the new economic and institutional framework if certain deficiencies are not corrected that have ballasted the running of the Spanish economy in the past. The transformations that will accompany the UME suggest that this will have serious effects on the behaviour of the economy.

In the first place, as the possibility of carrying out devaluations does not exist, the weight of the adjustment (in the presence of disequilibriums) will fall in an immediate and direct way on the real variables, if there is not a sufficient degree of flexibility of prices and wages. In fact, the existence of the exchange rate has served (worked) as an insulator against exterior influences, allowing, the accommodation of the domestic disequilibriums generated by the inefficiencies in the running of the productive system. These inefficiencies have been located traditionally in the market of factors (rigidity of the labour market) and in the goods market (strongly protected sectors from the competition and where there are companies that have an important market power) or like in certain spheres of public activity (tendency to an insufficient budgetary discipline, lack of cost rationalisation and lack of structure in the public sector).

In this context, in order to obtain the potential benefits of the EMU, it is required that the agents of the economy adapt their attitudes to the new environment. There are some elements that could prevent the running of the economy within the EMU: the coexistence of sectors protected and exposed to the competition with different behaviours; the existence of regional disturbances and the problems of the labour market; the possible processes of space concentration, etc. These circumstances could also happen outside the EMU, but the respond capacity through the traditional instruments (exchange rate, fiscal and monetary policy) will be seen to be drastically limited within it.

The essential question that must be answered is how will the EMU overcome these structural ties. The previous experiences advise certain caution at the time of judging the adaptation capacity of the Spanish economy. The Spanish economy has undergone two great transformation and liberalisation processes in the last decades (the Plan of stabilisation in 1959 and the entrance in the European Community in 1986). Although, these two processes were accompanied by high growth rates, they did not help overcome some of the main problems of the economy. With respect to the past, nevertheless, the Monetary Union offers an important qualitative change, in the sense a significant reduction of the margin available to accommodate the disequilibriums takes place. In the past the use of the exchange rate and other instruments has protected, sometimes, the existence of inefficiencies. We can hope that the Monetary Union provides an incentive to adapt the productive attitudes of the agents and the productive structures to the new, more competitive framework.

Secondly, to avoid the risk of the European Union (when promoting the market's integration) releasing that underlying tendencies that could end up in a divergence process (which could be harmful to Spain), it is essential to improve the Spain's capacity to incorporate itself in the group of more dynamic and advanced economies. These improvements must be destined to increase the technological, infrastructure and human capital endowment. This has to be done in order to get the maximum benefit from the Spanish comparative advantages. The larger space concentration that will probably generate the greater integration, the world-wide expansion process of the economy, the increasing competition of emergent markets and the future integration perspectives of the East countries in the European Union, make an effort to intensify the technological development necessary, in order to balance out Spain's level of economy with that of the central countries of the Union.

Both processes (the adaptation to the new environment and the effort to improve the productive capacity of Spain), must be run in a parallel way and must be framed in a coherent economic policy design. The objectives that, nowadays, the economic policy faces, go beyond the fulfilment of the convergence criteria to enter in the EMU. The essential factor is that the Spanish economy must still approach substantial tasks that it allow to overcome definitively the structural ties of its economy and to make the EMU benefits totally effective. However, the success of the adaptation to the new economic environment, will only be possible with the support of the society. The first step to obtain this is to understand the implications that the entrance in the Monetary Union holds.

We will finish this dissertation by looking at Intra-Union exports and imports of EU countries. We do this in order to see if Spain (and EU countries) would benefit from a monetary union. Let us first introduce some data on the importance of intra-EU trade for each EU country.

Table 4.3: Intra-Union exports and imports of EU countries (as per cent of GDP) in 1995:

Descargar

| Enviado por: | Andoni Abio |

| Idioma: | inglés |

| País: | España |

Todos los derechos reservados.