Economía y Empresa

Information Systems of Bancaja

Index

What is BANCAJA?…………………………………………………………………….…3

Where BANCAJA operates?………………………………………………….………...…4

Resources Employed ………………………………………………………………………6

Information Systems ………………………………………………………………………7

Internet …………………………………………………………………………………….9

Intranet …………………………………………………………………………………...10

Phone calls ……………………………………………………………………………….13

Physical mail……………………………………………………………………………...13

Fax………………………………………………………………………………………...14

BANCORREO……………………………………………………………………..……..14

Meetings………………………………………………………………………………..…14

TL4………………………………………………………………………………………..15

References………………………………………………………………………………...16

Information Systems of BANCAJA

What is BANCAJA?

BANCAJA is a non-profit financial organization that combines the social spirit of savings organizations with the management criteria of commercial banks.

Its fullname is Caja de Ahorros de Valencia, Castellón y Alicante (the saving Bank of Valencia, Castellon and Alicante). It's a financial organization that has been part of the history of the Valencian Community for over a century and a half, an organization which has always made and continues to make a significant and growing contribution to both the economic and social development of the region.

BANCAJA's aims, amongst the others is:

-

To facilitate the formation and capitalization of savings.

-

To administer the resources that it is entrusted with and make these productive.

-

To provide a full range of financial services to meet its customers' requirements.

-

To make productive investments that contribute to the increase of wealth and economic development in its region of activity.

-

To promote social activities that contribute to improving the quality of life and assist cultural and social progress in its operating region.

Four Competitive advantages help maintain BANCAJA's leadership within its area of activity:

-

Its expensive commercial presence, including a complete network of service points.

-

An important body of two million customers.

-

Its highly qualified professional staff and the advanced technological level of its operating equipment.

-

The organization business strategy, which has clear objectives, and embraces different approaches to the different marketplaces.

The BANCAJA group is made up of:

-

The Caja de Ahorros de Valencia, Castellón y Alicante, BANCAJA, The result of the merger of four Valencian savings banks together with Sindibank.

-

Holdings in the Bank of Murcia and the Bank of Valencia, both of regional character.

-

Its operating companies, which are engaged in financial broking insurance, travel, operating services, valuation, repossession and property activities.

Majors Holdings of BANCAJA:

* Banks

-

Banco de Valencia 37'88%

-

Banco de Murcia 100%

* Insurance

-

Aseval 100%

-

Coseval 100%

-

Segurval 100%

-

Coseval II 100%

-

Consultora de Pensiones 100%

* Financial

-

Gebasa 100%

-

Bancaja International Capital 100%

-

Bancaja Eurocapital Finance 100%

* Property

-

Cisa 100%

-

Actura 100%

* Investment

-

S.B.B. Participaciones 100%

-

Valenciana de Inversiones Mobiliarias 100%

-

Vainmosa cartera 17'58%

-

Ribera Salud 33%

-

Cegas 9%

-

Terra Mítica 11'89%

-

Aguas de Valencia 2,33%

-

Aumar 1,89%

* Services

-

S.B. Activos 51%

-

Mercavalor 16,67%

-

Servicio telefónico G.B. AIE 95'14%

-

Grupo de Bancaja Centro de Estudios 100%

-

Cavaltour 50%

-

Agro-Caja Sagunto 100%

-

Key 34'99%

-

Acinsa 22'42

In terms of turnover BANCAJA is the largest financial organization in the Valencian Community, the fourth largest saving bank in Spain and the core of a corporate group with great development potential that is currently one of the country's ten largest financial organizations.

Where does BANCAJA operate?

Territory

The geographical setting for a people four million strong, known as the Valencian Community, is mid-way along the Spanish Mediterranean coast. This land of mountains and beaches, large inland valleys and coastal market gardens covers an area of 23.000 square kilometres.

The Valencian Community has large urban centres, surrounded by counties of diverse economic activity. Large towns and high population density 171 inhabitants per square kilometre- give this land a characteristic liveliness. BANCAJA is also present in others parts of Spain, and particularly, for reasons stemming freom the comtemporary history, in the region of Albacete, which belongs to the Castilla-La Mancha Autonomous Community.

BANCAJA has an extensive network of offices throughout the Valencian Community and Albacete, where it has a position of clear leadership. It also has offices in large towns in nine other autonomous regions that play a strategic part within the organization.

Customers

BANCAJA tries to satisfy the demand for the financial products and services of the most diverse social elements in its region of activity:

-

Households and individuals.

-

The medium and high-income bracket.

-

SMES (small and medium sized business) and shops.

-

Public and privates institutions.

Quality of service is a basic premise in the business strategy established by BANCAJA, for whom the customer is the key to success.

Foreign Markets

-

Loans are issued on European markets through subsidiary companies.

-

Co-operation agreements on technology, sales strategy and charity projects with a variety of organizations in Europe and America.

-

BANCAJA was the first Spanish savings bank to be authorized to operate in the United States, which it now does through its branch in Miami, Florida.

Resources Employed

A great staff.

BANCAJA has 4.400 professionals looking after its wide-ranging and varied network of service points.

First-class computer equipment.

BANCAJA has extensive and effective computer equipment, with applications specially designed for financial entities. The computer centre also handles the Bank of Murcia's operations. The central system is based on a IBM S/930 system and other equipment.

Connected to these computers are:

-

More than 3500 teleprocessing terminals.

-

1300 personal computers with a local intercommunication links.

Information Systems of BANCAJA

BANCAJA is an organization with many departments. BANCAJA controls a lot of kind of firms too. So it's like a big firm with different goals. To run the firm and get all those goals, BANCAJA has to control and distribute the flow of information.

In BANCAJA, we can find a lot of ways of communication, between the different levels. There are several employees in BANCAJA who works far away from the others and they need the information quickly to be efficient.

Structure: The Managing structure of BANCAJA is a hierarchical structure; all the employees are subjected to their manager, and also the manager is subjected to another. That can cause problems of communication. When the employees need an approval from their manager or from other partner, they have to wait for it. BANCAJA has tried to solve it with the horizontal lines, with phone calls, or intranet.

Technology adaptation: In the last years, BANCAJA´s policy has been pointed to renew the staff, to change, to prepare the new staff to be able to work. It has brought BANCAJA to go a higher position because the problem to adapt the staff to the new technologies has been quicker. The reason of this better adaptation has been that younger people are more prepared to the new technologies.

Security in the Information Systems: `most every financial institution across the country - and probably throughout the world - has a detailed plan for what to do in case of an in-person robbery. However, fewer than 2% of financial institutions worldwide have developed an internal security policy that specifies the steps employees should take when suspicious activity is detected with regard to the institution's computer systems.

The fact is, there is a limited number of people who have the capability to rob a financial institution in person. However, there are potentially millions of people who have the capability to cause mischief by computer. Over 80% of the threat to an institution's systems comes from its own employees: current, former and contract. No system is completely safe. As has always been the case, security technology and criminals are in a never-ending race, each trying to outsmart the other.

BANCAJA has dedicated a lot of money to reduce the possibilities of risk of a hacker robbery, but it's impossible to eliminate all the risks.

Also, BANCAJA has made structure changes in the buildings to reduce the possibilities of the physical robberies. For example: every employee who uses money works behind a glass window between the worker and the clients. Also BANCAJA has changed the places of the safety boxes, which were close to the walls because there were a lot of robberies in Spain that thieves used to crash a car against the wall, breaking the safety box and stealing the money.

To make this changes, BANCAJA hasn't waited the robbery happens, BANCAJA has investigated to find the most efficient plan. An internal security plan should address at least four issues:

-

Risk identification-knowing your systems well enough to know where its weaknesses are,

-

Break-in prevention-developing a strategy for addressing your systems' weaknesses and "plugging the holes,"

-

Break-in recognition-being able to tell when a breach has occurred, and

-

Damage control-minimizing the damage in the event of a breach or disruption.

Most importantly, the plan should name one person as the plan's administrator-one person who is ultimately responsible for the system and its safety. It is important that only one person act as administrator for two main reasons: first, if a crisis should occur, one person should have the authority to act immediately without having to call a committee together or wait for approval from someone else; second, one person should be ultimately responsible for clearing employees for various levels of security. If too many people make security clearance decisions, then the security of the entire system is jeopardized.

Finally, the plan should rely on the expertise and experience of your employees for success. You may have hardware and software in place to help monitor security, but it is ultimately the employees who use the system that know where its weaknesses are.

Ways of Information: BANCAJA has made a completed net of communication about all the workers. Inside of it we can find:

-

Internet

-

Intranet

-

Phone calls

-

Physical mail

-

Fax

-

Bancorreo (Bane-mail)

-

Meetings

-

Its own information program called TL4

Internet

Every worker has for his disposition a computer connected to the net. Workers use it to find every kind of information to help us to work more efficiently.

The main utility of Internet is the relationship we can find between BANCAJA with clients and BANCAJA with suppliers. That relationship is built with a solid communication. BANCAJA has put, at the disposal of clients and suppliers, every type of information that they need. They can observe and operate with their accounts and they can do every kind of transactions on them. BANCAJA give a “Digital PIN (digital personal identify number)”, to authorize clients or suppliers to operate with the accounts.

Also they can establish a communication with the Bank, using the e-mailbox, but they'd better to use instant messages, to create an intranet net communication.

All that information has to be safe. We have to emphasize in the security again. We can distinguish Confidentiality and Security.

Security. Security is to be able to put your money in the bank, and keep it safe, as well physically as in Internet. Also it's important to keep the bank operation system safe, avoiding anybody can make mischief in the accounts or in the system. Internet has opened a big door to the hackers to operate widely and with all kind of freedom. BANCAJA, (like the others banks), has spend a lot of money to find the best way to keep the money safe. (For example: A few years ago, “Citybank” suffered three important robberies of millions of dollars.)

Confidentiality. Not only the money is important. There is a lot of information about the clients and about the own firm that has to be filed without risk. (Addresses, accounts, private files…). Directly connected with the flow of information is the matter of privacy: the growth of information technology and the increase of information in decision making are today more than in the past forces that threaten the privacy of the costumers. LORTAT (Ley de Ordenacion de Datos de Caracter Personal= Personal Character Data Ordination Law) is the law that regulates the privacy rights.

To find that security and confidentiality a lot of firms have changed their information systems, they have changed to an intranet net communication.

Intranet

An important reason to put Intranet in BANCAJA is the reduction of the costs. Also it's very important to save time, and time is money. Employees spend a lot of time answering routinely asked questions. The solution to solve this problem is to put the information on an Intranet. Not only to put it out there, refer all your callers to your Intranet. For example: Before your travel office answers the phone play a short recorded message saying "For routine questions check our pages on the company Intranet at www..... ."

The one problem with using email is that the entire message is usually not conveyed in the first communication. One email usually starts a string of emails back and forth until the other part completely understands your request or message. Instead consider putting forms on your Intranet.

Intranet has been a very good advance, and it has been accepted very well. It has caused a big reduction in the information costs of teamwork and hence makes it a more efficient solution to the organizational design problem. With intranet you can send every kind instant message (internal e-mail).

Also it's possible to left messages in accounts. That's very useful, because that message appears everywhere the client is. For example: If there is a person who has been several times a slow paying client, It's possible to put a message announcing to be careful with him (or refusing to give money to him). If the client use his notebook (Its like the credit card. The difference is that the movements are written in the notebook) or his card, the message will appear in the computer.

Although Intranet has increased the flow of information, a big problem has appeared. The flow of information has been so overloaded that people can't attend to all of it. To solve this problem, the employees use to make phone calls for the most important.

It exists a workgroup, who sends to the appropriate employees, everyday, some messages about the changes of the market, or the changes of the environment. Every BANCAJA worker use to receive some documents like the following:

-

Commercial Documents: Those documents use to orient the employees to work efficiently, (what to do?)

-

Marketing plan: Every year a marketing plan is created to instruct the employees how to sell the products. Here, the employees can find the marketing goals.

-

Products and Prices: Here, the employees can find all the changes about the different products (loan, fixed rate investments, variable rate investments…) and prices (%, formalization costs, initiation costs).

-

Negotiation tools: Every client, depending his likes, dislikes, money, investments… has a preferences. When the client goes to the bank, the employee knows all of those preferences because he receives short messages about the client. For example: An old man who has a lot of money in a account. Our employee should advice him to do an investment.

-

Market Tendencies: The bank advises the employees what they used to do, or to advise to the clients, about the changes of the market.

-

Competition Informs: They talk about the results of the different bank competitors: their changes, their innovations.

-

Commercial Planning Manual: It's a complete guide that explains how to act, to convince the clients, and the best way to do it.

-

Operative Documents: After the negotiation, we have to know how to carry out the formalization of the contracts. (How to it?)

-

General Communications: Here, the employee can find all kind of information about the computer operation system.

-

Procedure Manual and Codes Manual: They are two big and complete guides that explains how to create the product in the operate system, and to save the operation in the computer files. There is a guide to solve the easier problems too.

-

Products and Services Prices: Here, we can find the news and how to consult and how to operate with the bank products and bank services.

-

Support Office: There is a workgroup whose mission is to help and solve the more complicated branch problems.

-

General help: That kind of messages tries to help in the following cases: 1.rates informs. 2.fraud informs, (For example: If there are some thieves and they have stolen with success some banks, an internal message is sent to every branch who is situated in that region. 3. Signs. (Digital signs). 4.Operation Guide changes. 5. All about foreign money and their changes. 6. Fiscal Information. 7. Solidarity accounts 8. New computing versions. 9.Offices and Automatic Teller Machines nets. 10. Offices Platform. 11. Peripherals.

-

Negotiation reports: Those reports talk about the present and the future economic situation.

-

Annual Memory: Those documents contain documents about the Accounting (Balance, Financial Statement…), and the economic situation of the firm.

-

Firms Rates and Services Level Indicators: They are very useful to compare with the other branches results. There are a lo t of kind of indicators: Human Resources, Juridical Services, Marketing and Commercial Management, Alternatives Ways Management, Real Exterior Business Management, Technical Resources Management, and Control and Financial Management Indicators.

-

Technical Area Projects and CIN: Centro de Información Contable= Account Information Center: They are development centers that try to find a better way to minimize the costs and maximize the profit.

-

Communications

-

First Page: It's a summary with the most important news of BANCAJA.

-

News Summary: It's a summary about the most important economic news.

-

Monthly Magazine and Interviews: More complementary information about the most important event that happens in the firm.

-

Service Petitions

-

How to consult and to do Central services petitions.

-

Central services Petitions Statistics.

-

Process

-

Opening and Closing Offices. Summary of the new offices, and changes.

-

Offices Specialization. Made for the firms.

-

Buildings Promoter Division. Made for the promoter clients.

-

Personal Bank Division. Made for the high income clients

-

Commercial Bank Division. The rest of the clients.

-

Human Resources

-

Formation Center. BANCAJA makes Courses and Guides to the young people who want to work in BANCAJA. Also BANCAJA has Formation Offers and Professional Ways.

-

Evaluation Center. This center evaluates if all kind of goals have been kept and how they have been done.

-

Personal Data Consulting. Here, every worker can find all the information about his partners. (Workplace, permissions…). Also there is some information about the Medical Services, a behaviour guide…

Phone calls

Every worker has his own telephone. There is a internal line to talk with the partners of the same branch. There are more two or three telephone numbers in each office (Manager phone number, Employees phone number, general phone number).

Physical mail

The physical mail is only used in specific situations. Most of the activities, that mail was used, have been changed to the BANCORREO (BANE-MAIL). Here there are some examples of its utility. At the last page we can find a picture of the physical mail structure. (page n.16

-

Income: Everyone who wants to put money into an account belonging to another person will get a receipt. The income will be registered in the computer and another receipt will go to the owner mailbox by the physical mail. The bank use to do it with the wedding accounts, school accounts etc…

-

Credit: The bank only uses the physical mail when the client is from a different branch and he complains to his branch office that he hasn't made that credit. Example: client who lives in Algemesi and has his account in the 111.branch from Algemesi. He went to Pedreguer to visit some friends and he went to the bank and he took money from the 289.branch, in Pedreguer. He came back and a few days after, he looked his movements and he didn't remember to do that credit. He went to complain to the 111.branch in Algemesi. The employee can watch that he did that credit, but if he can prove it, he has to ask for the original paper (signed by the client), which is in Pedreguer. Then, the employee will have to use the physical mail.

-

Banker's order or bank transference: It's like incomes, but the last receipt is sent to the other bank, not to the owner of the account (because the owner of the account is not a BANCAJA client).

-

To increase or decrease the rights and duties: A long years ago the only place where you can change your rights and duties it was in the branch that you had been registered. But that has been changed. You can change it in every branch of the bank, but after the bank has to send the sign to the branch where the client pertain to be filed. For example: if a client wants his girlfriend to take money from his account, he can make the order in every branch.

-

Loan: That case is more complicated. The highest position of the branch has to enough qualified to make loan. If the employee can't make loans or big loans, it will be more costly. The employee has sent it to the manager; the manager has to approve it. Finally the manager will send it again to the original branch.

-

Cheques, letters of change, promissory notes… A that kind of paper money has to be approbated by the client branch. First of all, the employee has to receive the phone call approbation, after he has to send the original paper (by physical mail) to the client branch to be filed.

-

Investments (and bonds…): All kind of investments uses the same process like loans.

Fax

Every office has a fax. The most important function of the fax is the possibility to send a copy of the cheques to receive the approval from the manager. This only happens if the cheque hasn't been truncated (more than 10 millions de ptas. 556000 Swedish Kronor aprox.)

BANCORREO (BANE-MAIL)

It's the substitute of the mailbox; it's an internal and instant mail. Every time is more used by the BANCAJA workers.

Meetings

There are: annual meetings (Everybody has to turn up), trimester meetings (Every manager has to turn up), monthly meetings (Manager with the Negotiation Unit), and weekly meetings (Manager with his workers).

Its own information program called TL4

TL4 is a complete operation system that permits to carry out all the bank functions. Every short period of time (every week) there are new changes, to try to do a more perfect system. Those changes are not big, to avoid the confusion of the employees.

Every operation is made in the computer is filed in a memory daily. It's also filed, every thing about who has made it, when, where, and the results .All the computers are connected and it's possible to get all kind of information of every client.

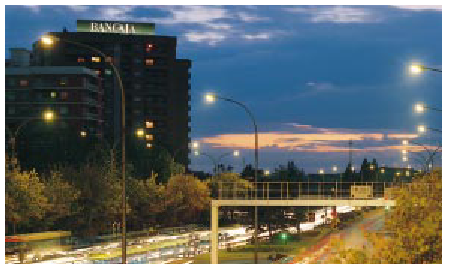

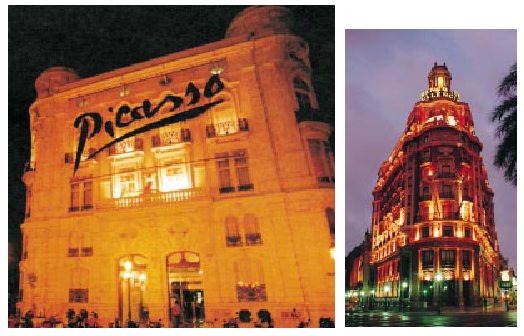

To end our work, we would like to show a picture gallery and the Central Bank, both are situated in Valencia. The first picture is an important building in Valencia, where BANCAJA assign part of its money to make social works. The second picture is a night view of the Central Bank of BANCAJA in Valencia.

References:

From the staff of the bank:

Documents and information

From the literature:

-

”Information System and the Organization of Modern Enterprise”, Brynjolfsson and Mendelson

-

“Four Ethical Issues of the Information Age”, Richard O. Mason

-

“Employee-propelled information provision”, Carl-Johan Petri

From the Internet:

-

www.competia.com

:

:

Branches send the information to their central operator, which distribute it to the final destination's central operator. Finally, the information is delivered to the final destination. BANCAJA

16

PERSONAL MAIL

BRANCH A

BRANCH B

BRANCH C

VALENCIA

ALICANTE

VALENCIA

ALICANTE

CASTELLON

CASTELLON

BRANCH E

BRANCH D

NACIONAL &

INTERNATIONAL

NACIONAL &

INTERNATIONAL

Descargar

| Enviado por: | Fernando Lluch Iborra |

| Idioma: | inglés |

| País: | España |

Todos los derechos reservados.